Project Samara: Canada’s First Tokenized Bond Experiment Explained

Project Samara is a landmark Canadian capital-markets experiment that brought together the Bank of Canada, Export Development Canada, RBC Capital Markets, RBC Investor Services and TD Bank Group to test how tokenized bonds could work in practice. In March 2026, the group completed Canada’s first tokenized bond issuance using distributed-ledger technology and settled payments with wholesale central bank deposits. That combination matters: it moved the discussion beyond theory and into a live, regulator-supervised market test. This article explains how Project Samara was designed, what it achieved, where the risks remain, and what it could mean for the future of tokenized securities in Canada.

Why tokenized bonds are gaining attention

Bond markets are large, essential and often operationally complex. Issuance, allocation, settlement, custody, coupon processing and redemption usually involve multiple intermediaries, separate records and time delays between trade execution and final settlement. That structure works, but it can be costly, fragmented and slow to adapt. Tokenization is being explored as a way to represent bonds digitally on a distributed ledger, allowing ownership and cash movements to be coordinated on a shared infrastructure.

For central banks and major financial institutions, the appeal is straightforward. A tokenized bond system can potentially support near-instant settlement, better data consistency, more transparent recordkeeping and automated lifecycle events such as coupon payments and redemption. In a market where failed reconciliations, settlement lags and duplicated processes still create friction, these gains are meaningful.

Canada did not begin this journey with Samara. The Bank of Canada had already explored distributed-ledger technology through earlier Jasper projects, which examined how wholesale payments and securities settlement could work on new digital rails. Internationally, markets have also been testing similar ideas. Switzerland’s SIX Digital Exchange is one of the most visible examples of a regulated environment for digital securities, while European authorities have pushed experimentation through the EU’s DLT Pilot Regime. These efforts share a common goal: modernize market infrastructure without undermining stability, trust or regulatory oversight.

What makes tokenized bonds especially interesting is that they sit at the intersection of traditional finance and digital infrastructure. Unlike many crypto-native assets, bonds are familiar instruments with well-understood legal and economic characteristics. That makes them a practical test case. If a market can prove that a bond can be issued, traded, settled and redeemed more efficiently on DLT, it creates a template for wider adoption across other securities.

Project Samara was designed to test exactly that question in a controlled, institutional setting rather than in a public, retail-facing market.

How Project Samara worked

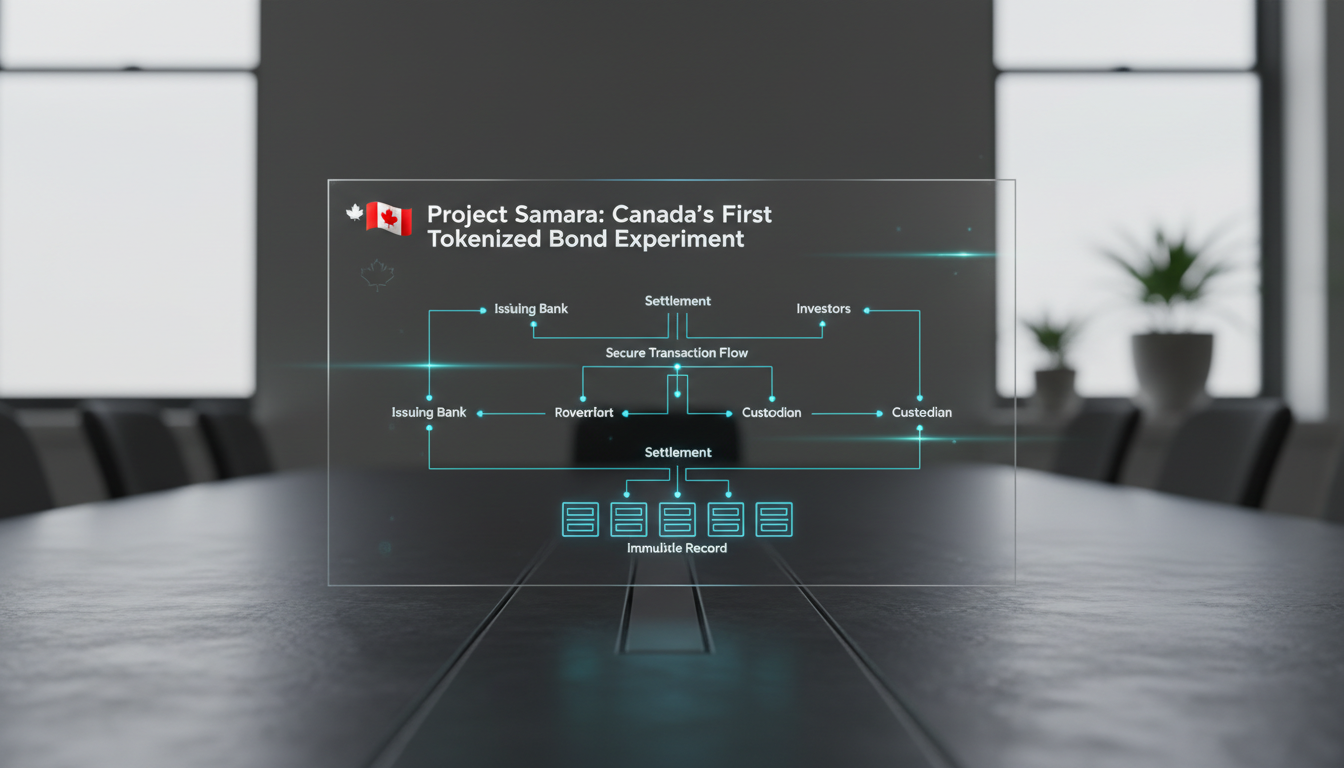

At the center of Project Samara was a C$100 million three-month tokenized bond issued by Export Development Canada. The experiment was conducted on the Samara Platform, a distributed-ledger environment built on Hyperledger Fabric. Rather than tokenizing a bond in isolation, the platform brought together both the bond ledger and the cash ledger so the full transaction cycle could be tested in one environment.

The workflow went beyond simple issuance. The platform supported the key stages of the bond lifecycle, including issuance, bidding, coupon processing, redemption and secondary trading. That breadth is important because many proofs of concept focus on one narrow function. Samara tested whether a tokenized security could move through multiple real market processes using the same digital infrastructure.

Settlement was completed using wholesale central bank deposits. This was a critical design choice. It meant the payment leg did not rely on a public blockchain token or private stablecoin. Instead, the cash side used a form of central bank-backed wholesale money suited to institutional testing. That made the experiment more relevant to regulated capital markets, where settlement finality and credit quality are central concerns.

Participation was limited to a closed group of institutional investors. The bond was not offered to retail investors, and the network was not an open public marketplace. This restricted structure reduced legal and operational uncertainty while allowing the project team and regulators to observe how tokenized bond infrastructure performs under controlled conditions.

The participants each played distinct roles. EDC acted as issuer. RBC Capital Markets and TD Bank Group were among the major dealers involved in the testing. RBC Investor Services contributed to the market-infrastructure and servicing side. The Bank of Canada supported the experiment by enabling the use of wholesale central bank deposits for settlement. Taken together, the project represented collaboration across issuer, dealers, infrastructure providers and public-sector institutions.

That collaborative structure is one reason Project Samara drew so much attention. It was not simply a fintech demonstration. It was a coordinated test involving institutions that already shape Canada’s financial plumbing.

The technical architecture behind the Samara Platform

The Samara Platform was built on Hyperledger Fabric, a private permissioned DLT framework commonly used for enterprise blockchain applications. Hyperledger Fabric differs from public blockchains in several important ways. Access is restricted to approved participants, identities are known, governance rules are defined in advance and transaction privacy can be structured according to institutional needs. For an experiment involving regulated securities and wholesale settlement, those features were more suitable than a public network.

In practical terms, the platform integrated two core digital records: one for the bond itself and one for the cash used to settle transactions. This matters because delivery-versus-payment is one of the hardest parts of securities settlement. If both the asset and payment leg are represented on coordinated ledgers, the system can reduce timing mismatches and lower settlement risk. Tokenization also supports more direct lifecycle management. Coupon events, maturity payments and ownership changes can be reflected on-chain, reducing the need for manual reconciliation across separate systems.

The choice of a permissioned network also helped address confidentiality and compliance concerns. Bond-market participants generally require clear controls over who can view data, who can validate transactions and how records can be audited. A private institutional network provides that structure more easily than a fully open blockchain.

Using wholesale digital dollars instead of public stablecoins was another deliberate decision. Stablecoins may be useful in some digital-asset markets, but they introduce their own credit, reserve and regulatory questions. In contrast, wholesale central bank deposits align more naturally with the needs of high-value institutional settlement. Project Samara therefore tested tokenized bonds in a framework closer to the standards expected in mainstream capital markets.

The result was not a claim that all securities markets should immediately move on-chain. Rather, it was a technical demonstration that a bond can be digitally issued and serviced on a controlled ledger where cash and securities interact in a more synchronized way than in many legacy systems.

What the project found: efficiency gains and real obstacles

Project Samara identified genuine benefits. The experiment showed that tokenized infrastructure can improve operational efficiency and strengthen data integrity by reducing duplication and making records more consistent across participants. When a shared ledger becomes the common source of truth, fewer reconciliations may be needed between institutions maintaining separate databases.

Another benefit was the reduction of counterparty and settlement risk. If the cash and bond legs move together through a coordinated system, the window in which one party has delivered while the other has not can be reduced. In traditional markets, even highly reliable settlement systems still involve process steps and timing structures that create friction. Tokenization offers a path toward more immediate finality.

Still, the experiment also underlined the limits of the technology. One of the most important findings was that efficiency gains in one layer can be offset by complexity elsewhere. New infrastructure must be integrated with existing systems, compliance frameworks and operational processes. Market institutions do not replace core infrastructure lightly, especially when current systems are deeply embedded and trusted.

Liquidity costs and governance requirements also emerged as challenges. A tokenized market needs rules for participation, access, servicing, record ownership, incident response and dispute handling. In a closed pilot, these questions can be managed through project governance. At scale, they become harder. Market operators need clarity over roles that are routine in conventional finance but less settled in tokenized environments.

The project also highlighted new operational risks. While distributed ledgers may reduce some traditional forms of settlement risk, they create dependence on software design, network permissions, cybersecurity controls, auditability processes and fallback arrangements. A market must know what happens if a node fails, a smart workflow malfunctions or a participant loses connectivity during a critical event. These are not theoretical concerns; they are central to whether institutional markets can trust a new settlement layer.

Another practical barrier is institutional appetite. Many market participants may support innovation in principle while remaining cautious about large-scale changes to core systems. That caution is rational. Capital markets depend on reliability. For tokenized bonds to move beyond pilots, they must prove not only that they are faster or cleaner, but that they are operationally resilient and commercially worthwhile.

The table below summarizes the balance Project Samara revealed between promise and implementation risk.

| Observed advantage | Why it matters | Main challenge |

|---|---|---|

| Faster settlement | Reduces exposure between trade and final payment | Requires integration with existing systems and processes |

| Shared data integrity | Lowers reconciliation burdens across institutions | Needs strong governance and audit standards |

| On-chain lifecycle automation | Can streamline coupon and redemption workflows | Creates dependence on software reliability and fallback design |

| Lower counterparty risk | Improves confidence in securities settlement | Liquidity and market-depth questions remain |

The broader lesson is clear: tokenized bonds are not just a technology upgrade. They require coordinated changes across infrastructure, regulation, governance and market behavior.

Regulatory oversight and the CIRO sandbox

Project Samara did not take place in a legal vacuum. The testing occurred under regulatory supervision, including approval from the Canadian Investment Regulatory Organization through its InnovateSafe sandbox. CIRO authorized RBC and TD to test tokenized bonds using wholesale digital dollars in a controlled setting, which gave the experiment a defined compliance perimeter.

This matters because one of the biggest questions around tokenized securities is not whether the software works, but whether the activity can fit into market rules designed for traditional financial instruments and intermediaries. Sandbox structures allow regulators and firms to test real use cases while limiting scale, monitoring risks and gathering evidence before broader approval is considered.

Under this model, participating dealers are expected to file regular reports on risk and performance. Further use of the private blockchain infrastructure would require additional approval. That approach reflects a cautious but constructive regulatory stance: encourage experimentation, but do not assume that a successful pilot automatically justifies market-wide deployment.

The Bank of Canada’s role was also specific. It supported the use of wholesale digital dollars for settlement in the experiment. This is distinct from any debate around a retail central bank digital currency. Wholesale digital money is aimed at institutional settlement and market infrastructure. Retail CBDC discussions concern public access to digital central bank money for everyday payments. Project Samara belongs firmly in the wholesale category.

That distinction is important for readers who might confuse tokenized bond settlement with consumer-facing digital currency projects. Samara was about capital-markets plumbing, not retail wallets or public token spending.

Benefits, risks and how Samara compares with other DLT experiments

The benefits of tokenized bonds, as demonstrated or suggested by Project Samara, are easy to understand in market terms:

- Near-real-time settlement instead of traditional settlement delays.

- Improved transparency and data integrity through synchronized records.

- Reduced counterparty risk when payment and securities move together.

- Programmable automation for coupons, redemption and servicing.

- Potential long-term cost savings from simpler post-trade workflows.

RBC and EDC executives pointed to the experiment as a practical example of innovation through institutional collaboration. That is a meaningful point. Tokenization in regulated markets is unlikely to scale through isolated pilots alone. It requires alignment between issuers, dealers, service providers, regulators and central-bank-linked settlement systems.

But the risks remain substantial. Operational complexity, cybersecurity exposure and auditability demands all rise when markets depend on new digital infrastructure. Governance questions also become sharper. Who operates the marketplace? Who acts as custodian? How are records recognized across legal and accounting frameworks? How are incidents handled? These issues are manageable in a pilot, but much harder in a mature market.

Liquidity is another concern. A tokenized bond may be technically elegant while still trading in a thin market. Without broad participation and integration into existing workflows, tokenized instruments can remain niche products with limited depth. That in turn reduces their usefulness for issuers and investors.

Compared with earlier Jasper experiments in Canada, Project Samara pushed the concept further into tokenized securities issuance and lifecycle management. Jasper explored wholesale payments and settlement concepts that laid important groundwork. Samara applied similar institutional DLT thinking to a live bond-use case with a defined issuance and investor process. Internationally, it resembles other private permissioned initiatives, such as Swiss digital-bond infrastructure and European pilot programs, but differs in its specific use of wholesale central bank deposits and the structure of Canadian regulatory supervision.

The comparison below shows where Samara fits in the wider DLT landscape.

| Initiative | Primary focus | Network style | Settlement approach |

|---|---|---|---|

| Project Samara | Tokenized bond issuance and lifecycle testing | Private permissioned | Wholesale central bank deposits |

| Bank of Canada Jasper projects | Wholesale payments and settlement experimentation | Institutional DLT testing | Wholesale-focused concepts |

| SIX Digital Exchange | Regulated digital securities infrastructure | Permissioned institutional | Digital market settlement framework |

| EU DLT Pilot Regime | Regulated experimentation in tokenized financial markets | Controlled market pilots | Varies by venue and structure |

The common pattern is experimentation within regulated or semi-regulated institutional environments, not open public issuance at mass scale. That tells us where the market is today: interested, serious and still cautious.

What tokenized bonds could mean for investors and Canadian markets

For now, Project Samara is mainly relevant to institutional investors, dealers and market-infrastructure specialists. Retail investors could not buy the bond used in the pilot. Still, the long-term implications go beyond wholesale finance. If tokenized securities infrastructure matures, smaller institutions and eventually retail users could gain access to more efficient digital bond markets with fewer intermediaries and faster settlement.

That does not mean a sudden shift to fully on-chain retail fixed-income trading. A more realistic path would be gradual expansion: more pilots, additional asset classes, deeper legal clarity and more standardized servicing models. Over time, tokenized bonds could also interact with other digital-finance systems, including on-chain collateral management, tokenized deposits or selected DeFi-style infrastructure built to institutional standards.

Canada’s broader financial modernization efforts could eventually support that direction. Improvements in real-time payments infrastructure and progress in consumer-driven banking may help create an environment where digital financial products become easier to connect, move and verify. But market readiness will matter as much as technology. Institutions adopt new infrastructure slowly when legal certainty, interoperability and liquidity remain uncertain.

For readers who want to monitor this area, the smartest approach is to follow official sources closely. Updates from the Bank of Canada, CIRO, RBC, EDC and Payments Canada will provide the clearest signals about whether tokenized bond testing expands into new products or market structures.

If you are comparing where digital assets or future tokenized products may eventually be accessible, start by using regulated venues and doing proper platform research. CoinixPro offers a useful way to compare crypto exchanges before choosing a provider. Readers who are newer to the space can also build their foundation through crypto guides for beginners. And if you want a broader look at reputable services, CoinixPro’s overview of the best crypto platforms can help you narrow your options responsibly.

A simple way to stay informed is to follow a structured checklist:

- Watch official announcements from the Bank of Canada and CIRO.

- Track whether new pilots include other securities or investor groups.

- Check how settlement is handled: wholesale deposits, tokenized deposits or other forms of digital cash.

- Review whether the trading venue and custody model are regulated.

- Compare platforms carefully before using any digital-asset service.

Conclusion

Project Samara marks a significant step in Canada’s exploration of tokenized securities. It showed that a tokenized bond can be issued, settled and serviced on institutional DLT using wholesale central bank deposits, but it also made clear that efficiency gains come with governance, integration and operational challenges. The experiment’s biggest contribution may be its realism: it treated tokenization as market infrastructure, not hype. If Canada continues pairing innovation with strong regulatory coordination, it could play a leading role in the next phase of digital finance.

FAQ about Project Samara

What is Project Samara?

Project Samara is Canada’s first major tokenized bond experiment involving the Bank of Canada, Export Development Canada, RBC Capital Markets, RBC Investor Services and TD Bank Group. It tested whether a bond could be issued, traded and settled on distributed-ledger technology within a regulated institutional framework.

What bond was issued in the experiment?

EDC issued a C$100 million three-month tokenized bond as part of the pilot. The issuance was used to test the full process around digital bond creation, bidding, settlement and lifecycle servicing.

Who participated in Project Samara?

The experiment involved EDC as issuer, major financial institutions including RBC and TD, RBC Investor Services, and the Bank of Canada in its wholesale-settlement role. Participation was limited to a closed group of institutional participants rather than the general public.

Was the tokenized bond available to retail investors?

No. The Samara bond was not open to retail investors. It was a controlled institutional test designed to evaluate market infrastructure, compliance and settlement mechanics in a restricted environment.

How does tokenized settlement work in Project Samara?

In the experiment, both the bond and the cash leg were represented within a coordinated DLT environment. This made it possible to manage delivery-versus-payment more directly, reducing the gap between transfer of the bond and final transfer of cash.

What technology did the platform use?

The Samara Platform was built on Hyperledger Fabric, a private permissioned DLT framework. It was chosen because it supports known participant identities, controlled access, enterprise governance and privacy features better suited to regulated capital markets than public blockchains.

Why were wholesale central bank deposits used instead of stablecoins?

Wholesale central bank deposits are more aligned with institutional settlement needs because they are linked to central bank money and fit more naturally into regulated financial-market infrastructure. Public stablecoins can raise additional issues around reserves, credit quality and regulation.

What are the main benefits of tokenized bonds?

The key potential benefits include faster settlement, lower counterparty risk, stronger data integrity, more transparent records and automation of bond lifecycle events such as coupon payments and maturity redemption.

What risks did Project Samara highlight?

The experiment highlighted operational complexity, cybersecurity concerns, auditability challenges, governance requirements, fallback design issues and possible liquidity limitations. It also showed that integration with existing market infrastructure remains a major hurdle.

Did Project Samara prove that tokenized bonds are ready for mass adoption?

No. It showed that tokenized bond infrastructure can work in a controlled setting, but it did not prove that broad adoption is immediate or inevitable. Scaling the model would require more regulatory clarity, stronger interoperability, deeper market participation and confidence in the operating model.

How is Project Samara different from the Bank of Canada’s earlier Jasper work?

Jasper focused more broadly on wholesale payments and settlement experiments. Project Samara applied similar institutional DLT thinking to a more specific securities use case by testing the issuance and servicing of a tokenized bond.

How does Project Samara compare with global tokenized bond initiatives?

It shares important features with other international pilots, especially the use of private permissioned infrastructure and a regulated environment. Its distinguishing feature is the Canadian institutional setup and the use of wholesale central bank deposits in the settlement framework.

What role did CIRO play?

CIRO approved RBC and TD to test tokenized bonds using wholesale digital dollars within its InnovateSafe sandbox. This gave the project a regulated testing environment and required ongoing reporting on risks and performance.

Is Project Samara related to a retail CBDC in Canada?

No. Project Samara involved wholesale digital money for institutional settlement. That is different from a retail central bank digital currency, which would be aimed at consumers and everyday payments.

Could tokenized bonds eventually connect with DeFi or other on-chain systems?

Potentially, yes, but that would likely happen gradually and under tighter controls than in open crypto markets. Institutional-grade tokenized bonds could eventually interact with tokenized collateral systems, tokenized deposits or selected on-chain financial infrastructure if regulation and market design evolve in that direction.

What should investors watch next?

Investors should watch for new pilots, expansion into other asset classes, clearer rules for custody and trading venues, and signs that tokenized settlement can integrate more smoothly with existing infrastructure. Official communications from the Bank of Canada, CIRO, EDC, RBC and Payments Canada will be the most useful sources.