Crypto Remittances to Southeast Asia: Using Stablecoins for Cheaper Transfers from Singapore

Crypto remittances Singapore is becoming a practical topic for migrant workers, freelancers, small businesses and digital-first users who regularly send money from Singapore to Southeast Asia. Singapore acts as a financial hub and employment base for people supporting families, contractors and suppliers in the Philippines, Indonesia, Vietnam, Malaysia, Thailand and Cambodia.

Traditional remittance providers move money through banks, agents, payment processors and foreign exchange desks. That structure can create transfer fees, FX markups and settlement delays. Stablecoins offer another route: a sender converts Singapore dollars into a fiat-backed digital token, transfers it over blockchain rails, and the recipient converts it into local currency. The model can reduce costs, but the real outcome depends on platform fees, liquidity, regulation, wallet security and local off-ramp access.

What Are Crypto Remittances?

Crypto remittances are cross-border money transfers that use digital assets instead of relying only on banks or traditional money transfer operators. In the context of stablecoin remittance Singapore users are usually not trying to speculate on crypto prices. They are trying to move value from a sender in Singapore to a recipient in Southeast Asia with lower friction.

This distinction matters. Bitcoin and many altcoins can fluctuate significantly between the time a sender transfers funds and the time a recipient cashes out. Stablecoins are designed to track fiat currency value, such as the US dollar or Singapore dollar. For remittance purposes, value stability is more useful than price volatility because the recipient usually wants Philippine pesos, Indonesian rupiah, Vietnamese dong, Malaysian ringgit, Thai baht or Cambodian riel at the end of the transfer.

A stablecoin remittance uses three basic entities: a sender, a wallet and a recipient. The sender funds an account in Singapore, buys a stablecoin, sends it across a blockchain network, and the recipient uses an exchange, wallet or off-ramp provider to convert the stablecoin into local fiat currency.

Why Traditional Remittances from Singapore Can Be Expensive

Traditional remittance services charge more than one visible fee. A Singapore to Philippines transfer may include a fixed transfer fee, an exchange rate spread and a cash pickup charge. A Singapore to Indonesia transfer may include platform fees and a markup between the displayed SGD/IDR rate and the wholesale market rate. A Singapore to Vietnam crypto remittance may look attractive only if the recipient can cash out cheaply into Vietnamese dong.

The cost stack usually includes several layers. A remittance provider charges a fixed fee for processing the transaction. The provider may also apply an FX markup when converting Singapore dollars into PHP, IDR, VND, MYR or THB. If a bank or intermediary payment network handles part of the settlement, another cost may appear. If the recipient chooses cash pickup, the receiving side may also charge a service fee.

Small transfers are hit harder because a fixed charge takes a larger percentage of the total amount. A S$200 transfer can feel much more expensive than a S$2,000 transfer when the same fixed fee applies. For migrant workers sending family support, freelancers receiving project payments and small businesses paying regional vendors, this percentage cost can matter more than the headline fee.

Speed is another issue. Bank transfers and agent-based remittances may settle in hours, but some corridors still take one or more business days. If the transfer involves compliance checks, weekends or multiple intermediaries, the recipient may wait longer than expected.

How Stablecoins Can Reduce Remittance Costs

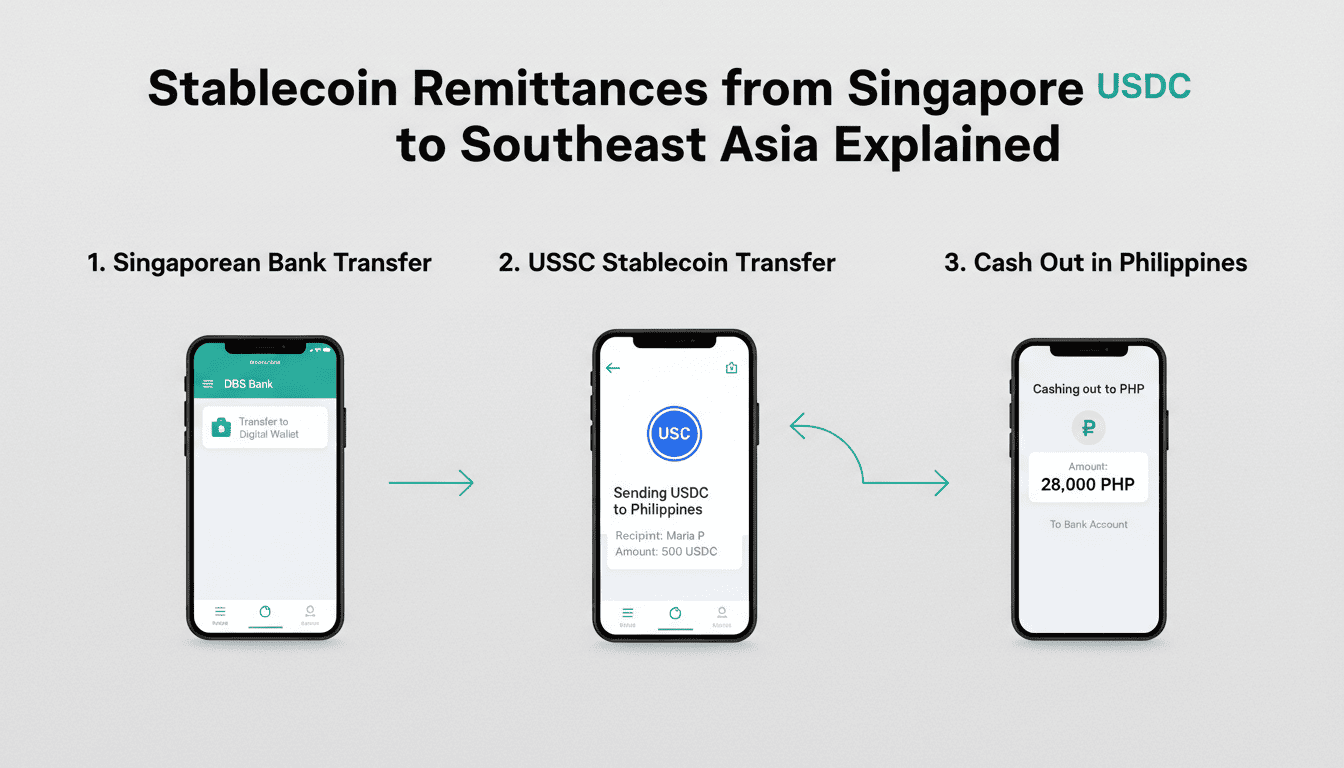

Stablecoins can reduce remittance costs because they move value directly over blockchain networks. Instead of depending on multiple correspondent banks or cash pickup agents, a Singapore-based sender can convert SGD into a stablecoin and transfer it to a recipient wallet. The recipient then converts the stablecoin into local currency through a supported exchange, wallet, peer-to-peer marketplace or local off-ramp provider.

A typical stablecoin transfer from Singapore works like this:

- The sender funds an account with Singapore dollars.

- The sender buys a stablecoin such as XSGD, USDC or USDT.

- The sender transfers the stablecoin to the recipient’s wallet address.

- The recipient converts the stablecoin into local currency.

- The recipient spends, withdraws or transfers the local funds.

This process can be cheaper when the blockchain network fee is low and the destination country has strong stablecoin liquidity. Layer 2 networks may reduce on-chain costs further, especially for frequent small transfers. However, a stablecoin transfer is not automatically the cheapest option. The total cost includes network fees, platform trading fees, deposit fees, exchange rate spread, withdrawal fees and off-ramp charges.

The off-ramp is often the deciding factor. A Singapore to Philippines crypto transfer may be fast on-chain, but the recipient still needs reliable PHP cash-out. A Singapore to Indonesia stablecoin transfer may depend on IDR liquidity and local exchange support. A Singapore to Vietnam crypto remittance may work better for a digital-native recipient than for someone who needs immediate cash pickup.

For readers comparing digital asset platforms, it can be useful to understand how Singapore’s crypto market infrastructure is developing. CoinixPro’s overview of Singapore’s flexible crypto capital framework for banks provides additional context on how digital asset services may interact with the regulated financial sector.

Stablecoins Used for Remittances from Singapore

XSGD

XSGD is a Singapore-dollar-linked stablecoin that represents SGD value on blockchain rails. For Singapore-based senders, XSGD can be useful when they want digital value denominated in Singapore dollars before converting to another currency. StraitsX provides resources on XSGD and related digital payment infrastructure, which can help users understand how SGD-linked tokens are used in practice.

XSGD remittance is most relevant when the platform supports SGD deposits, XSGD conversion and onward transfer. The recipient’s country must still support a practical conversion route. If a recipient in Indonesia, Vietnam or the Philippines cannot easily convert XSGD into local fiat, the sender may need to use a more liquid stablecoin.

USDC

USDC is a USD-backed stablecoin commonly used for digital dollar transfers and global liquidity. For USDC remittance Singapore users, the main advantage is broad exchange support. Many exchanges, wallets and payment platforms support USDC pairs, and the stablecoin is designed to track the US dollar through reserve-backed issuance.

USDC may be suitable when the destination off-ramp supports USD stablecoins and offers reasonable conversion into PHP, IDR, VND, MYR or THB. Users should still check network support because USDC exists on multiple blockchains, and sending it to the wrong network can result in lost funds.

USDT

USDT is widely used across Asia because it has deep liquidity and broad exchange availability. USDT remittance Asia corridors can be practical when the recipient’s local platform supports USDT deposits and cash-out into domestic currency. This liquidity can make USDT useful for frequent cross-border payments, contractor payments and small business transfers.

Users should still review platform support, issuer information, network fees and redemption conditions. A widely used stablecoin can still carry platform, custody and compliance risk if the sender or recipient uses an unreliable provider.

Local or Regional Stablecoins

Regional stablecoin experiments include tokens linked to local currencies, such as Indonesian rupiah-linked stablecoin models or XIDR-style concepts where available. These can be useful only when liquidity, compliance and platform support exist. A local-currency stablecoin may sound ideal for a Singapore to Indonesia stablecoin transfer, but it is only practical if the recipient can receive, trade and cash out the token at a reasonable cost.

Example Corridors: Singapore to Southeast Asia

Singapore to the Philippines

The Philippines is a major remittance market, and many Singapore-based workers send regular family support to recipients who need Philippine pesos. A stablecoin transfer from Singapore to Philippines may help when the sender wants faster digital settlement and the recipient has access to a supported wallet or exchange.

The practical question is not only whether the sender can buy USDC, USDT or XSGD in Singapore. The recipient must also cash out to PHP. If the recipient uses a local exchange, mobile wallet integration or cash-out partner with reasonable fees, stablecoins may reduce the total cost. If the recipient needs physical cash immediately and has no wallet experience, a traditional remittance operator may still be more convenient.

Singapore to Indonesia

A Singapore to Indonesia stablecoin transfer can be relevant for workers, vendors, small businesses and regional sellers. The sender may choose USDT or USDC if those stablecoins have better IDR liquidity on the recipient’s preferred platform. XSGD may be useful at the Singapore funding stage, but conversion into Indonesian rupiah depends on the available exchange route.

IDR cash-out is the key bottleneck. The recipient should confirm whether a local exchange, wallet or payment service supports the chosen stablecoin and blockchain network. If a local-currency stablecoin is available, it may simplify accounting, but only if spreads are tight and withdrawal options are reliable.

Singapore to Vietnam

Singapore to Vietnam crypto remittance use cases often involve freelancers, contractors, family support and digital-native users. A Vietnamese recipient who already uses crypto wallets may receive stablecoins quickly and convert them through available channels. For remote teams, stablecoin cross-border payments may also simplify recurring payments when both sides understand wallets and network selection.

Local conversion remains essential. The sender should ask whether the recipient can convert USDC or USDT into Vietnamese dong without excessive spread or withdrawal friction. A low on-chain fee does not help if the final cash-out cost is high.

Singapore to Malaysia and Thailand

For Singapore to Malaysia and Singapore to Thailand transfers, stablecoins may be useful for fast settlement, business payments and digital freelancers. However, nearby regional corridors may already have competitive bank transfer, fintech app or e-wallet options. The sender should compare the total transfer cost rather than assuming that blockchain remittance Singapore routes are always cheaper.

Stablecoins can still be attractive for users who make frequent payments outside business hours, manage cross-border invoices or need transparent transaction records. Traditional fintech apps may be better when the recipient wants simple local currency delivery without managing private keys or exchange accounts.

Stablecoins vs Traditional Remittance Services

The table below compares traditional remittance services with stablecoin remittance from Singapore. The best option depends on the recipient’s access, the corridor’s liquidity and the total cost after conversion.

| Factor | Traditional Remittance | Stablecoin Remittance |

|---|---|---|

| Transfer speed | Hours to several days | Minutes or near-instant |

| Fees | Fixed fee + FX spread | Network fee + platform/off-ramp fee |

| Access | Bank, agent, app | Wallet, exchange, digital platform |

| Transparency | FX markup may be unclear | On-chain transfer is traceable |

| Volatility | Fiat-based | Lower if fiat-backed stablecoin is used |

| Main bottleneck | Intermediaries | Off-ramp and compliance |

| Best for | Cash pickup and non-crypto users | Digital users and frequent transfers |

Stablecoins can be cheaper when a corridor has strong liquidity and reliable off-ramp access. Traditional remittance services can be more suitable when the recipient wants cash pickup, does not use digital wallets or needs a familiar customer service channel.

How to Send Money from Singapore Using Stablecoins

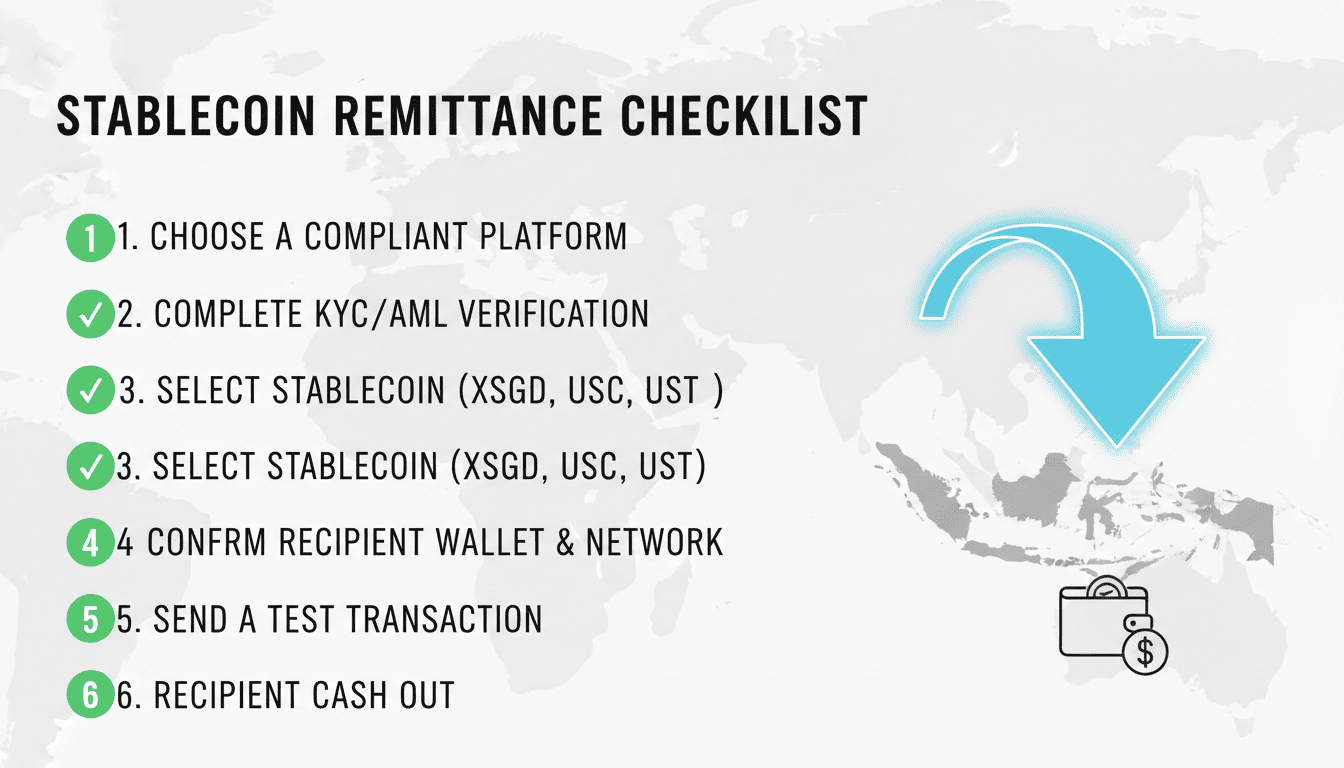

Step 1: Choose a Compliant Platform

The sender should use a provider that supports SGD funding and follows Singapore compliance standards. A compliant platform helps users deposit Singapore dollars, buy stablecoins and transfer funds with clearer processes. Readers comparing digital asset platforms can also review AI crypto trading tools and platform access in Singapore to understand how account access, tools and user onboarding are evaluated in the local market.

Step 2: Complete KYC

KYC verification is normal for regulated payment services. Platforms use identity checks to comply with AML requirements, reduce fraud and confirm that users are allowed to access digital payment token services. Singapore-based users should expect to provide identification and account details before sending larger amounts.

Step 3: Buy the Right Stablecoin

The sender should choose XSGD, USDC or USDT based on the route, fees and recipient’s cash-out options. XSGD may suit SGD-denominated value. USDC and USDT may provide deeper liquidity in some Southeast Asian markets.

Step 4: Confirm the Recipient Wallet and Network

The sender must confirm both the wallet address and blockchain network. USDC or USDT sent on the wrong network may be difficult or impossible to recover. The recipient should provide the exact address for the selected network.

Step 5: Send a Small Test Transaction

A small test transfer reduces operational risk. If the recipient receives the test amount and confirms cash-out access, the sender can send the remaining balance with more confidence.

Step 6: Recipient Converts or Spends the Stablecoin

The recipient may use an exchange, wallet, peer-to-peer marketplace or local off-ramp. The final result depends on local fiat withdrawal options, exchange spreads and available banking or wallet integrations.

Key Risks to Understand Before Using Stablecoin Remittances

Off-Ramp Risk

The recipient may receive stablecoins but struggle to convert them into local currency. Off-ramp risk is often the biggest practical constraint for crypto money transfer Southeast Asia corridors.

Network Risk

Stablecoins exist on multiple blockchain networks. A sender who chooses the wrong chain may lose access to the funds. Confirming the network before sending is essential.

Platform Risk

Users should check whether a platform is reputable, secure and compliant. Custody arrangements, withdrawal rules and customer support affect the user experience.

Stablecoin Issuer Risk

Fiat-backed stablecoins depend on reserves, redemption policies and issuer transparency. Reserve-backed stablecoins are generally more suitable for remittance use than algorithmic stablecoins because the sender and recipient need predictable value.

Regulatory Risk

Rules differ across Singapore, the Philippines, Indonesia, Vietnam, Malaysia, Thailand and Cambodia. A service available in one country may not support the same features in another country.

Wallet Security Risk

Private keys, seed phrases and account passwords control access to funds. Users should secure wallets, enable authentication tools where available and avoid sharing recovery phrases.

What MAS Regulation Means for Stablecoin Remittances in Singapore

The Monetary Authority of Singapore regulates payment services and digital payment token services under Singapore’s financial framework. MAS focuses on consumer protection, AML/KYC controls, technology risk and the conduct of payment service providers. Users can review official information on MAS payment services regulation and MAS stablecoin framework developments for broader context.

For stablecoin payments Singapore users, regulation affects how platforms onboard customers, monitor transactions and manage risk. KYC checks help platforms comply with AML requirements. Licensed providers may offer clearer processes, but users should still check whether a provider is licensed, regulated or otherwise allowed to offer digital payment token services in Singapore.

MAS has also discussed reserve and redemption expectations for certain stablecoin arrangements. This matters because stablecoin remittances depend on confidence that the token represents fiat value and can be redeemed or exchanged through supported channels.

Who Can Benefit Most from Stablecoin Remittances?

Migrant workers can benefit when stablecoins reduce the cost of sending regular family support from Singapore to the Philippines, Indonesia or Vietnam. A lower fee on repeated transfers can create meaningful savings over time if the recipient can cash out affordably.

Freelancers and remote contractors can benefit when stablecoins provide faster cross-border payments than bank wires. A designer in Vietnam, a developer in the Philippines or a vendor in Indonesia may prefer digital settlement when both sides understand wallets and conversion routes.

Small businesses can use stablecoin cross-border payments to pay suppliers, regional sellers and contractors. The advantage is strongest when payment timing matters and the receiving party already uses an exchange or digital wallet.

Digital-native users benefit most because they can manage wallet addresses, network selection and off-ramp choices. Stablecoin remittance is less suitable for recipients who need immediate physical cash and have no access to reliable digital platforms.

Practical Checklist Before Sending a Stablecoin Remittance

- Is the platform available in Singapore?

- Does it support SGD deposits?

- Which stablecoin is supported: XSGD, USDC, USDT or another token?

- Which blockchain network is used?

- Can the recipient cash out locally into PHP, IDR, VND, MYR, THB or another currency?

- What is the total cost after platform fees, network fees, FX spread and off-ramp charges?

- Is the recipient comfortable using a wallet or exchange account?

- Has a small test transfer been completed?

- Are KYC requirements clear for both sender and recipient?

- Is the stablecoin fiat-backed, liquid and widely supported?

This checklist helps Singapore-based users compare stablecoins for remittances against banks, e-wallets and traditional remittance providers. The cheapest-looking route is not always the cheapest after cash-out.

Future of Stablecoin Remittances in Southeast Asia

Stablecoin remittances from Singapore to Southeast Asia may become more useful as payment infrastructure improves. More fintech integrations, better wallet design and stronger compliance tools can make digital money transfer Singapore corridors easier for everyday users.

Regional stablecoin experiments may also develop alongside instant payment systems and tokenized money initiatives. If local-currency liquidity improves, a sender may have more practical choices beyond USD stablecoins. However, availability will vary by country, provider and regulation.

Research from sources such as the World Bank Remittance Prices Worldwide database and regional crypto adoption analysis from Chainalysis shows that cross-border payment cost, access and adoption remain important topics across emerging markets. Stablecoins are unlikely to replace every remittance provider immediately, but they may become an important alternative for digital-first users and high-frequency cross-border payments.

The next stage will likely depend on compliant off-ramps. If recipients in the Philippines, Indonesia, Vietnam, Malaysia, Thailand and Cambodia can convert stablecoins into local currency cheaply and reliably, stablecoin remittance Singapore use cases will become more practical.

Conclusion: Crypto Remittances Singapore and the Practical Role of Stablecoins

Crypto remittances Singapore can reduce the cost and settlement time of sending money from Singapore to Southeast Asia when stablecoins are used carefully. XSGD can represent Singapore dollar value on-chain, while USDC and USDT may provide broader liquidity for international transfers.

The real cost depends on off-ramp access, local liquidity, platform fees, network fees, FX spread and compliance requirements. Singapore-based senders should compare stablecoins with banks, e-wallets and remittance operators before choosing a route. A small test transfer, a compliant provider and a confirmed recipient cash-out method can make the process smoother.

For Singapore-based users who regularly send money across Southeast Asia, stablecoin remittances are worth understanding — not as a hype trend, but as a practical payment rail that may reduce costs when used carefully.

FAQ

Are stablecoin remittances legal in Singapore?

Stablecoin remittances may be available through platforms that comply with Singapore rules for digital payment token services and payment services. Users should check whether a provider is licensed, regulated or otherwise allowed to offer relevant services in Singapore.

Are stablecoins cheaper than traditional remittance services?

Stablecoins can be cheaper, but they are not always cheaper. The total cost depends on network fees, platform fees, FX spread, liquidity and off-ramp charges in the recipient’s country.

Which stablecoin is best for sending money from Singapore?

The best stablecoin depends on the corridor. XSGD may be useful for SGD exposure, while USDC and USDT may have deeper liquidity in some Southeast Asian markets. The recipient’s cash-out options should guide the choice.

Can I send stablecoins from Singapore to the Philippines?

Yes, a Singapore to Philippines crypto transfer is possible if the recipient has access to a supported wallet or platform and can convert the stablecoin into PHP at a reasonable cost.

What is the main risk of using stablecoins for remittances?

The main risks are off-ramp availability, wrong-network transfers, platform risk and stablecoin issuer risk. A transfer may be fast on-chain but still difficult if the recipient cannot cash out locally.

Do recipients need a bank account?

Not always. Some recipients may use a wallet, exchange account, peer-to-peer marketplace or cash-out partner. However, a bank account or mobile wallet may still be needed for local fiat withdrawals.

Should beginners use stablecoins for remittances?

Beginners can consider stablecoins if they use platforms with clear instructions, compliance standards and customer support. They should start with a small test transfer before sending the full amount.