Project Guardian and Asset Tokenisation: What Singapore Investors Should Know

Project Guardian Singapore has become one of the most closely watched developments in the local digital-asset ecosystem because it connects asset tokenisation with regulated financial-market infrastructure. The Monetary Authority of Singapore (MAS) launched Project Guardian to explore the potential and realisation of tokenised real economy and financial assets, and the initiative now sits at the centre of Singapore’s institutional tokenisation strategy.

For investors, the key question is practical: how do tokenized assets Singapore initiatives affect access, liquidity, settlement and risk? Project Guardian aims to enhance liquidity and efficiency in financial markets through asset tokenisation, while related MAS initiatives such as Global Layer 1 Singapore and BLOOM MAS are designed to support common infrastructure and settlement standards. This guide explains what Singapore investors, wealth-management professionals, fund managers and accredited investors should know before assessing tokenized investments Singapore opportunities.

What Is Project Guardian?

MAS Project Guardian is a collaborative initiative between MAS, global regulators and financial-industry participants. MAS launched Project Guardian in 2022 to explore tokenised real economy and financial assets, and the initiative seeks to establish industry frameworks and standards that support responsible asset tokenisation Singapore use cases.

Project Guardian aims to enhance liquidity and efficiency in financial markets through asset tokenisation. The programme has expanded to more than 40 industry participants, which indicates that Singapore’s tokenisation work has moved beyond isolated proof-of-concept trials and toward broader operating models for regulated institutions.

The initiative connects banks, asset managers, market operators, custodians, token issuers and regulators. The Investment Association, IMAS, the UK Financial Conduct Authority and other international regulators collaborate with MAS to explore regulatory considerations, investor protection and responsible innovation in tokenized assets Singapore markets.

For local investors, Project Guardian is not simply a “crypto” experiment. Project Guardian creates a regulated framework for tokenised bonds, tokenised funds Singapore products, tokenised money market instruments and other real-world assets, while MAS coordinates policy, infrastructure and legal design to support institutional adoption.

The Building Blocks of Tokenised Finance

Singapore asset tokenisation initiatives are best understood as connected layers rather than separate announcements. Project Guardian focuses on the tokenised asset layer, Global Layer 1 focuses on shared infrastructure standards, and BLOOM enables settlement using tokenised bank liabilities, regulated stablecoins and central bank digital currencies.

The Tokenised Asset Layer: Project Guardian

Project Guardian supports workstreams covering tokenised bonds, funds, structured products and other real-world assets. The initiative tests how regulated institutions can issue, distribute, manage and redeem tokenised financial products while maintaining compliance, governance and investor-protection standards.

MAS expanded Project Guardian into legal structures, interoperability standards and operating models for tokenised finance. In November 2025, MAS released an operational guide for tokenised funds, and the guide standardises areas such as governance, net asset value calculation, transfer-agent processes and compliance controls.

For Singapore investors, the tokenised asset layer matters because it defines the product itself. A tokenised fund still needs a fund structure, an issuer, a custodian, a transfer process and redemption rules, while blockchain records provide a digital representation of ownership or rights linked to the underlying asset.

Global Layer 1 (GL1)

Global Layer 1 Singapore refers to a shared-ledger initiative launched in June 2024 to explore infrastructure standards for settlement, data formats and connectivity. GL1 focuses on the rails that allow tokenisation platforms, financial institutions and market infrastructures to communicate with one another.

Global Layer 1 supports cross-platform interoperability because tokenised assets need common standards to move efficiently between issuers, distributors, custodians and settlement venues. Without shared standards, tokenised funds and bonds may remain trapped inside separate platforms, limiting liquidity and reducing investor usefulness.

For wealth managers and fund managers, GL1 is significant because it may reduce operational fragmentation. A common ledger or common technical standard can help different institutions use consistent settlement logic, data fields and connectivity models for tokenized investments Singapore portfolios.

BLOOM

BLOOM MAS is the settlement-asset layer introduced in October 2025 to support real-time and cross-border settlement. BLOOM enables settlement using tokenised bank liabilities, regulated stablecoins and CBDCs, which gives tokenised assets a safer and more efficient payment leg.

BLOOM supports tokenised assets by linking asset transfers with reliable settlement assets. When a tokenised bond or tokenised money market fund unit changes ownership, the cash leg can settle using digital money instruments that are designed for regulated financial-market use.

For investors, BLOOM matters because settlement quality affects execution, redemption and counterparty exposure. A tokenised investment may be efficient only if the asset token, cash token and legal claim operate together within a trusted and compliant settlement framework.

Tokenisation Explained: How Assets Become Digital

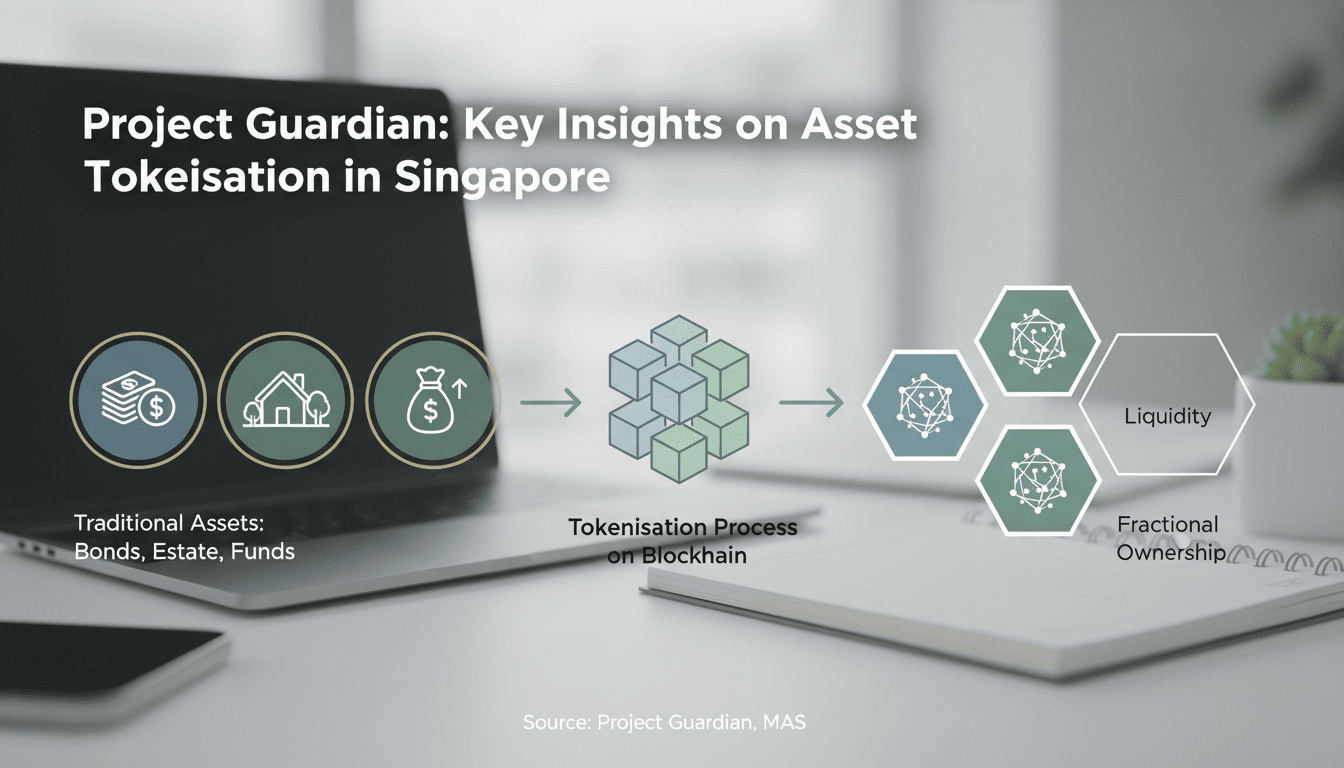

Asset tokenisation means converting ownership rights or economic interests in an asset into digital tokens recorded on a distributed ledger. The KPMG/SFA Asset Tokenization C-Suite Playbook describes tokenisation as a process that can enhance accessibility to investments and revolutionise the management of diverse asset classes.

Tokenisation can represent financial instruments such as bonds, equities and funds, as well as real assets such as gold, real estate and other real-world assets. Tokenisation allows fractional ownership because a high-value asset can be divided into smaller digital units that are easier to hold, transfer or trade.

For example, a traditional bond may require a relatively large minimum investment, while a tokenised bond may support smaller fractional positions if the issuer, platform and regulations allow it. Fractionalisation can broaden access, but investor eligibility, product suitability and platform rules still determine who can participate.

Tokenisation can improve transaction transparency because distributed ledgers record ownership transfers and transaction history. Smart contracts can automate settlement instructions, coupon payments, compliance checks or transfer restrictions, although the quality of those functions depends on the design of the underlying technology and legal framework.

For Singapore investors, the practical value of tokenisation lies in combining digital efficiency with regulated financial products. Asset tokenization enhances accessibility to investments, but the investor still needs to understand what the token represents, who holds the underlying asset and how redemption works.

Tokenised Products for Singapore Investors

Tokenized assets Singapore products are now moving from trials into more visible investor-facing examples. Singapore investors may encounter tokenised money market funds, tokenised funds, structured products and tokenised bonds, although access depends on whether the investor is retail, accredited or institutional.

Tokenised Money Market Funds

A tokenized money market fund Singapore product gives investors blockchain-native exposure to short-duration yield instruments. In November 2025, Franklin Templeton and DBS launched a tokenised money market fund for retail investors, which represents an important step in bringing tokenised funds Singapore products into mainstream banking channels.

The Franklin Templeton and DBS tokenised money market fund is structured under Singapore’s Variable Capital Company framework. The VCC structure provides a regulated fund vehicle, while DBS’s mobile banking app provides a familiar access point for eligible investors seeking short-duration investment exposure.

The product shows how tokenisation can sit inside a regulated distribution environment rather than outside the financial system. Tokenised fund units can provide transparent ownership records and fractional access, while the underlying money market portfolio remains governed by fund documentation, custody arrangements and redemption processes.

Investors should still review eligibility, fees, redemption timing and settlement mechanics. A tokenised money market fund for retail investors may be easier to access than institutional products, but it remains an investment product with terms that must be understood before subscription.

Tokenised Funds and Structured Products

MAS’s operational guide for tokenised funds, released in November 2025, standardises practical controls for fund tokenisation. The guide supports governance, NAV calculation, transfer-agent responsibilities, compliance monitoring and operational processes that tokenised fund issuers need before scaling regulated offerings.

InvestaX offers tokenised money market access and other tokenised investment products through a regulated marketplace model. A MAS-licensed Recognised Market Operator such as InvestaX can provide on-chain access to institutional-grade funds where the product structure, investor onboarding and secondary-transfer rules are defined.

Tokenised funds and structured products can broaden access to alternative investments, but many are currently limited to accredited investors. This means that how to invest in tokenised assets in Singapore often begins with investor classification, suitability checks and onboarding through a regulated platform or financial institution.

Tokenised Bonds

Tokenized bonds Singapore developments show how fixed-income markets may become more efficient through digital issuance and fractional ownership. OCBC launched bespoke tokenised bonds for corporate accredited investors in early 2025, giving eligible participants access to tokenised fixed-income exposure.

Tokenised bonds can streamline issuance because digital records can support subscription, ownership tracking, transfer restrictions and coupon distribution. A tokenised bond may also allow smaller positions than traditional private placements, although minimum size and eligibility depend on the issuer and offer structure.

Potential secondary liquidity is one attraction of tokenised bonds, but investors should not assume every token has an active market. The issuer’s credibility, the bond’s credit quality, the platform’s trading venue and the redemption terms all affect whether a tokenised bond can be sold or held efficiently.

Benefits of Asset Tokenisation for Investors

Asset tokenisation can enhance liquidity by allowing assets to be divided and traded in smaller units. Tokenisation benefits for investors are most visible when traditionally illiquid assets, such as private funds, bonds or fractional real-estate tokens Singapore products, become easier to access through digital distribution channels.

Fractional ownership gives investors access to assets that may otherwise require high minimum commitments. A high-value bond, real-estate interest or alternative fund can be represented by smaller tokenised units, although the platform and offer documents determine the actual entry threshold.

Efficiency is another benefit because smart contracts can automate selected operational processes. Tokenised funds and bonds can use programmable features such as automated coupon payments, transfer restrictions and settlement instructions, which may reduce manual reconciliation across issuers, custodians and transfer agents.

Transparency improves when tokenised ownership records are maintained on a distributed ledger. Investors, issuers and service providers may be able to view verified transaction histories, while compliance controls can restrict transfers to eligible investors.

Diversification is a practical reason to monitor tokenized investments Singapore opportunities. Tokenised products may give investors exposure to money market strategies, private-market assets, structured products or real-world assets, but benefits depend on platform maturity, regulatory compliance and market adoption.

Regulatory and Risk Considerations

Singapore asset tokenization regulation is shaped by MAS licensing, product rules and industry standards. MAS regulates digital payment token services and sets licensing requirements, while Project Guardian seeks to establish frameworks and standards for tokenisation in regulated financial markets.

The FCA collaborates with MAS to explore regulatory considerations for tokenisation. International regulator participation supports cross-border alignment because tokenised assets may involve issuers, investors, custodians and settlement assets across multiple jurisdictions.

Custody is a core consideration because investors need to know how tokens are held. A tokenised asset may sit in a custodial wallet managed by a regulated provider or, where allowed, a self-hosted wallet, and each model creates different responsibilities for private keys, access controls and recovery processes.

Settlement quality also matters because tokenised assets require a reliable payment leg. BLOOM enables real-time settlement using tokenised bank liabilities, stablecoins and CBDCs, but investors should understand which settlement asset is used and whether it is issued by a regulated or reserve-backed entity.

Redemption processes define how investors convert tokens back into fiat or redeem interests in the underlying asset. A tokenised money market fund, for example, may have cut-off times, valuation procedures and settlement timelines, even if the digital token transfer appears instant.

Liquidity should be assessed product by product because secondary markets for tokenised assets are still developing. A tokenised bond or fund unit may be technically transferable, but actual liquidity depends on buyer demand, platform rules, investor eligibility and market-making arrangements.

Counterparty risk remains relevant because tokenised ownership does not remove the need to assess issuers, custodians, transfer agents and service providers. Investors should evaluate the quality of the underlying asset, the legal enforceability of tokenised ownership rights and the credibility of the institution offering the product.

Technology and operational risks include smart-contract bugs, cybersecurity incidents, network downtime and integration failures. These risks can be reduced through audits, licensed intermediaries and institutional controls, but investors should still review the platform’s operational resilience before committing capital.

How Singapore Investors Can Participate

Singapore investors can participate in tokenised assets by first understanding their investor classification. Retail investors, accredited investors and institutional investors have different access rights, and many tokenised funds, structured products and tokenised bonds remain restricted to accredited or institutional investors.

Investors should choose regulated marketplaces or licensed financial institutions when assessing tokenised products. MAS-licensed Recognised Market Operators, licensed Capital Markets Services providers, bank distribution channels and regulated custodians can provide clearer compliance processes than unregulated channels.

Due diligence should focus on the underlying asset, issuer, custody setup, redemption terms and transfer restrictions. A token is only as useful as the legal rights it represents, so investors should review whether the token confers fund units, debt exposure, beneficial ownership or another contractual claim.

Fees also matter because tokenisation may reduce some operational costs but does not make investing free. Platform fees, custody fees, fund management fees, spread costs and network-related charges can affect net returns, especially for investors making smaller allocations.

The following checklist summarises practical questions Singapore investors can ask before entering tokenized investments Singapore products.

| Investor question | Why it matters |

|---|---|

| Am I retail, accredited or institutional? | Access depends on classification |

| Who issued the token? | Issuer quality affects enforceability |

| Who holds the asset? | Custody affects ownership protection |

| How do I redeem? | Redemption affects liquidity |

| Where can I trade? | Secondary markets may be limited |

A measured approach can help investors learn without taking excessive concentration risk. Investors can start with modest allocations, monitor MAS regulatory guidelines for tokenization and compare tokenised products with traditional funds or bonds before increasing exposure.

Future Outlook: 2025–2026 and Beyond

MAS’s vision for the next decade positions artificial intelligence and tokenisation as transformative themes for Singapore’s financial sector. The Singapore FinTech Festival 2025 discussion highlighted how Project Guardian Singapore, Global Layer 1 and BLOOM fit into a broader strategy for digital financial infrastructure.

Project Guardian is likely to expand as more banks, asset managers, market operators and regulators join the network. MAS has already expanded the initiative to more than 40 participants, and additional live trials may strengthen operating models for tokenised funds, bonds and settlement assets.

Live trials of tokenised MAS bills settled using CBDC could further demonstrate how tokenised public-sector instruments interact with digital settlement layers. These trials may help institutions test delivery-versus-payment models, settlement finality and interoperability across platforms.

Global momentum is also increasing because the Investment Association, IMAS and FCA are participating in tokenisation workstreams. International collaboration matters because capital markets are cross-border, and tokenised assets need common standards for issuance, distribution, custody and settlement.

Over time, tokenised assets may integrate with instant payment systems, regulated stablecoins and CBDC settlement rails. This could create more seamless cross-border investment flows, particularly for funds, money market instruments and bonds that require efficient settlement between institutional counterparties.

Tokenisation will likely not replace traditional markets overnight. Instead, asset tokenisation Singapore initiatives may become an important complementary channel for investors seeking operational efficiency, fractional access and diversified exposure through regulated digital infrastructure.

Conclusion

Project Guardian Singapore signals Singapore’s commitment to building a tokenised financial future through regulated collaboration rather than speculative hype. MAS launched Project Guardian to explore tokenised real economy and financial assets, and the initiative now connects asset design, infrastructure standards and settlement innovation.

For investors, the opportunity lies in understanding how tokenised money market funds, tokenised bonds and tokenised funds can improve liquidity, fractional ownership and operational efficiency. The responsibility lies in assessing custody, redemption, counterparty quality, eligibility and Singapore asset tokenization regulation before investing.

Singapore investors should monitor MAS announcements, product launches from regulated institutions and developments in Global Layer 1 and BLOOM. Before allocating capital to tokenised products, investors should consult qualified financial advisers and ensure each product matches their risk profile, liquidity needs and investment objectives.

FAQ

What is Project Guardian?

Project Guardian is a collaborative initiative led by MAS that explores the tokenisation of real economy and financial assets. Project Guardian aims to develop standards, frameworks and interoperable infrastructure that can support regulated tokenised finance in Singapore and across international markets.

How does asset tokenisation work?

Asset tokenisation converts ownership rights or economic interests in assets into digital tokens recorded on a distributed ledger. Tokenisation allows fractional ownership, transparent transaction history and programmable settlement, while the underlying asset remains governed by legal, custody and compliance arrangements.

What tokenised products are available in Singapore?

Examples include tokenised money market funds from Franklin Templeton and DBS, tokenised investment products from InvestaX and bespoke tokenised bonds from OCBC. Access depends on product licensing, platform rules and whether the investor is retail, accredited or institutional.

What are the benefits of investing in tokenised assets?

Tokenised assets may offer enhanced liquidity, fractional ownership of high-value assets, transparent settlement and broader diversification opportunities. These benefits depend on market adoption, platform maturity, regulatory compliance and the quality of the underlying asset.

What risks should investors consider?

Investors should consider custody arrangements, private-key controls, redemption terms, liquidity limits, counterparty quality, technology reliability and legal enforceability. A tokenised product can be regulated and innovative, but it still requires the same disciplined due diligence as any investment product.

Who can invest in tokenised products?

Access depends on investor classification and product structure. Some tokenised money market funds may be available to retail investors through regulated channels, while many tokenised funds, structured products and tokenised bonds are currently limited to accredited or institutional investors.

How is MAS regulating asset tokenisation?

MAS regulates digital payment token services, sets licensing requirements and leads Project Guardian to establish standards for tokenisation. MAS also works with international regulators such as the FCA to explore regulatory considerations, investor protection and responsible innovation in tokenised financial markets.