Fidelity Joins the Race for Stablecoin Reserve Management

Fidelity Joins the Race for Stablecoin Reserve Management

Fidelity Investments is preparing to enter the fast-developing market for stablecoin reserve management, according to a CoinDesk report on its June 17, 2026 announcement. The plan centres on a money market fund designed to hold reserve assets backing major stablecoins — a move that follows similar activity from State Street.

The news matters because stablecoins such as USDC, USDT and DAI sit at the centre of crypto trading, payments and blockchain-based finance. If large asset managers begin managing the collateral behind these tokens, the structure of the market could become more institutional, more regulated and potentially more transparent.

For UK readers following the latest crypto news, the Fidelity stablecoin reserves story is not just about one fund. It points to a broader contest between traditional finance, crypto-native issuers, regulators and investors over who controls the infrastructure behind digital money.

What Are Stablecoin Reserves and Why Do They Matter?

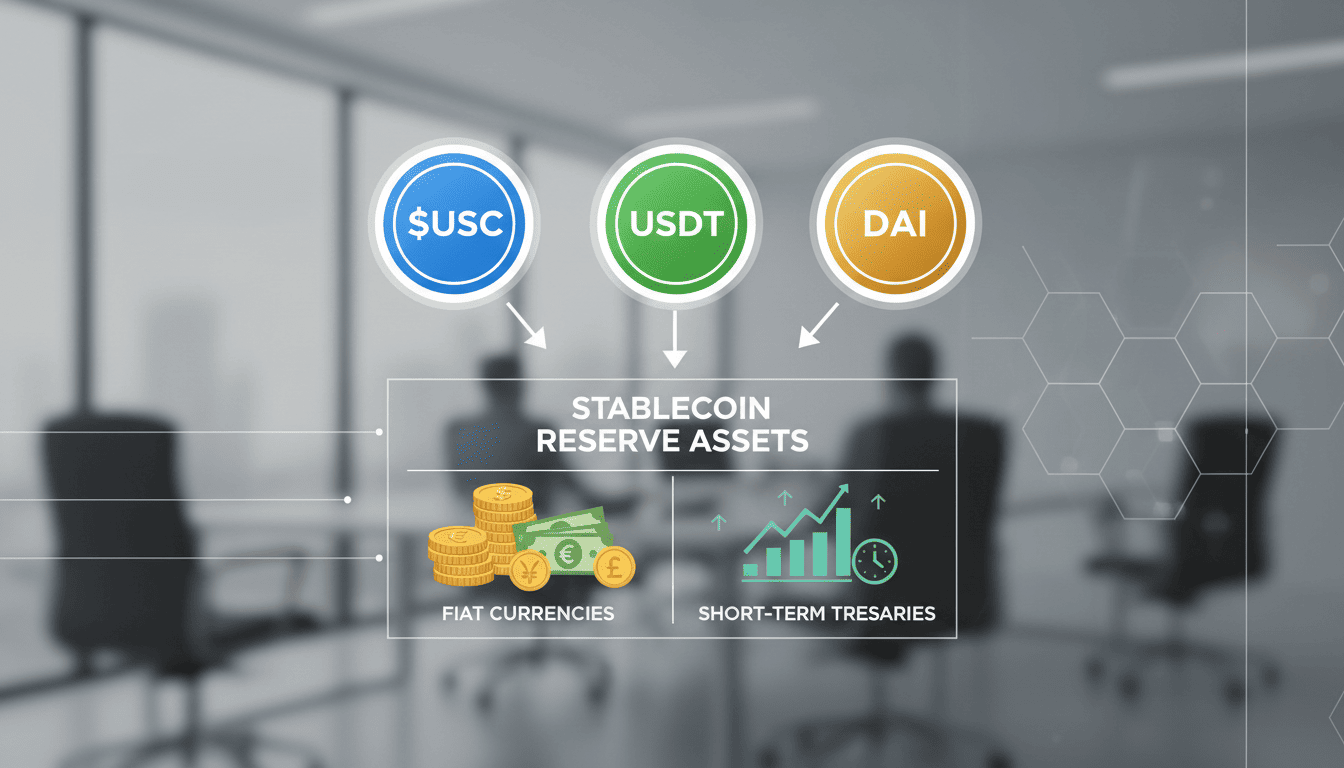

Stablecoins are crypto assets designed to maintain a stable value, usually by tracking a fiat currency such as the US dollar. To support that peg, issuers typically hold reserve assets. These may include cash, fiat-equivalent instruments, short-term treasuries or other collateral.

In simple terms, stablecoin reserves are the assets that give users confidence that one token can be redeemed for the value it claims to represent. If a stablecoin promises to track $1, users expect the issuer to hold assets sufficient to support redemptions when people want to exit.

Stablecoin reserve management is therefore a core part of the product, not a back-office detail. Poorly managed reserves can damage confidence, slow redemptions and put pressure on the peg. Well-managed reserves can improve transparency and make stablecoins more usable for payments, trading and institutional settlement.

USDC, issued by Circle, and USDT, issued by Tether, are among the most closely watched stablecoins because of their role across exchanges such as Coinbase, Binance, Kraken and Gemini. DAI, which is also widely used in decentralised finance, highlights how stablecoin collateral can vary depending on the design of the token.

A money market fund for stablecoins is relevant because these funds are commonly associated with short-duration, liquid instruments. In the context of stablecoin collateral, the appeal is straightforward: issuers need assets that can be managed conservatively and accessed efficiently during redemption periods.

That is why the Fidelity stablecoin reserves move is attracting attention. It brings a major traditional financial institution into a function that directly affects market trust.

Fidelity’s Entry Into the Stablecoin Reserve Market

Fidelity Investments plans to launch a money market fund aimed at holding assets that back stablecoins. The proposed Fidelity digital asset fund would place the firm alongside State Street, which has also moved toward stablecoin reserve management.

The attraction for traditional banks and asset managers is clear. The stablecoin market has grown into a major part of crypto infrastructure, supporting trading pairs, cross-border transfers, decentralised applications and institutional workflows. Even when investors are not buying Bitcoin or Ethereum directly, they may still use stablecoins to move in and out of positions.

For firms such as Fidelity Investments and State Street, stablecoin reserves represent a bridge between traditional money markets and blockchain-based finance. Reserve assets need custody, oversight, liquidity management and reporting — services that established financial institutions already understand.

The Fidelity stablecoin reserves strategy also reflects a wider shift in how traditional finance views digital assets. Rather than treating crypto only as a speculative market, large institutions are increasingly focusing on the plumbing: custody, settlement, collateral, tokenised funds and regulated access points.

State Street stablecoin reserves activity shows that this is not an isolated experiment. Other institutions, including J.P. Morgan and HSBC, are also part of the broader conversation around digital assets, tokenisation and payment infrastructure, even where their specific roles differ.

For stablecoin issuers such as Circle, Tether and PayPal, partnerships with large reserve managers could help address investor concerns about collateral quality, redemption processes and operational resilience. The trade-off is that crypto-native firms may become more dependent on traditional financial intermediaries.

Why This Matters for UK Investors

For UK investors, the Fidelity stablecoin reserves development matters because stablecoins are often used as a gateway between crypto markets and traditional currency. Even users who focus on Bitcoin or Ethereum may hold USDC, USDT or DAI temporarily while trading, transferring funds or waiting for market conditions to change.

The UK regulatory backdrop is still developing. The Bank of England has been consulting on the role of stablecoins in payments, including possible limits and safeguards. The Financial Conduct Authority is also expected to play a central role in oversight, depending on how UK crypto regulation is finalised.

That means UK investors and stablecoins are closely linked to questions of transparency. If a token is widely used, users need to understand what backs it, who manages those assets and how redemptions would work under stress.

The UK approach may differ from the United States, where agencies such as the US Federal Reserve, the Securities and Exchange Commission and other authorities influence the stablecoin debate. It also differs from the European Union, where MiCA has created a more defined framework for crypto assets, with a licence deadline expected in late June 2026.

Readers tracking UK crypto regulation should watch whether institutional reserve management becomes part of the policy discussion. A Fidelity-managed money market fund would not remove crypto risk, but it could become a reference point for what regulators expect from stablecoin collateral.

The Global Race to Set Stablecoin Rules

Stablecoins have become a regulatory priority because they sit between banking, payments, capital markets and crypto trading. They can move across blockchain networks quickly, but their value depends on off-chain reserve assets and redemption promises.

In the United States, the Federal Reserve and the SEC are part of the wider policy debate over stablecoins, market integrity and investor protection. In the European Union, MiCA is designed to create a common regulatory framework, with the European Central Bank also relevant to discussions about payments and financial stability.

The United Kingdom is taking its own path through Bank of England consultations and FCA oversight. The central question is how to regulate stablecoins without blocking useful innovation in payments, settlement and digital asset markets.

The Fidelity stablecoin reserves plan fits directly into this global race. If large asset managers take responsibility for reserve assets, regulators may have a clearer set of counterparties to supervise. That could make stablecoins easier to assess than arrangements where reserves are opaque or spread across less familiar structures.

At the same time, regulation will need to address how stablecoins interact with networks such as Ethereum, where tokens can be used in decentralised finance, trading, payments and smart-contract applications. The same token may be used by retail traders, institutions and automated protocols, which makes oversight more complex.

Clearer rules could benefit investors, issuers and asset managers. But until the UK, US and EU frameworks settle, stablecoin reserve management remains an area shaped by both commercial opportunity and regulatory uncertainty.

What It Could Mean for the Crypto Market

Greater participation from Fidelity Investments, State Street and other financial institutions could legitimise parts of the stablecoin market. Reserve management is not as visible as token launches or exchange listings, but it is central to whether investors trust stablecoins at scale.

For institutional investors, familiar names may reduce operational concerns. A stablecoin backed by assets managed through a recognised money market structure could be easier to evaluate than one with limited disclosure. That does not make the token risk-free, but it may make due diligence more straightforward.

Crypto-native companies may face new competition. Circle, Tether, PayPal and Coinbase all operate in parts of the stablecoin ecosystem, while exchanges such as Binance, Kraken and Gemini rely on stablecoins for liquidity and trading access. If reserve management becomes a specialised institutional service, fees and partnerships may become more important.

The development could also affect how users compare the best crypto platforms. Exchanges may increasingly compete not only on trading costs and coin access, but also on the quality of stablecoins they support, redemption transparency and banking relationships.

The Fidelity stablecoin reserves move therefore has implications beyond Fidelity itself. It may influence how stablecoin issuers choose partners, how regulators assess risk and how investors think about the difference between a token’s blockchain function and the assets backing it.

Risks and Caveats

Institutional involvement does not remove the risks around stablecoins. Concentration risk could increase if a small number of large asset managers control a significant share of reserve assets. That may improve professional oversight, but it could also create new dependencies.

Regulatory uncertainty remains another concern. UK rules, US policy and EU MiCA implementation may develop in different directions, creating complexity for issuers and investors who operate across borders.

There is also the possibility of conflicts of interest. If large financial institutions manage reserves, provide custody, support trading infrastructure or serve institutional clients, regulators and users will expect clear governance.

Most importantly, stablecoins still depend on confidence in the peg and the ability to redeem. If a stablecoin loses its peg, reserve quality, liquidity and market trust all come under immediate pressure.

What to Watch Next

The Fidelity stablecoin reserves story marks another step in the convergence of traditional finance and crypto infrastructure. Fidelity Investments is not simply entering a niche fund category; it is targeting one of the key mechanisms that allows stablecoins to function.

For UK investors, the main issues to watch are regulatory announcements from the Bank of England and FCA, the structure and transparency of Fidelity’s fund, and whether other banks or asset managers follow State Street’s lead.

Stablecoins are likely to remain central to crypto markets, but their future may depend less on branding and more on reserve quality, redemption processes and regulatory clarity.

Frequently Asked Questions

How will Fidelity manage stablecoin reserves?

Fidelity plans to launch a money market fund aimed at holding assets that back stablecoins. Based on the briefed announcement, the fund would focus on reserve assets rather than issuing a stablecoin directly.

What stablecoins are likely to be included?

The brief does not name specific stablecoins for Fidelity’s fund. Major stablecoins in the market include USDC, USDT and DAI, but any inclusion would depend on issuer arrangements and regulatory requirements.

Could UK investors access Fidelity’s stablecoin fund?

Access is not confirmed in the provided information. UK availability would likely depend on the fund’s structure, distribution permissions and how FCA and Bank of England rules develop.

How are stablecoin reserves different from bank deposits?

Stablecoin reserves are assets held to support redemption of a crypto token. Bank deposits are claims on a regulated bank account. The protections, oversight and legal structure may differ significantly.

What happens if a stablecoin loses its peg?

If a stablecoin loses its peg, users may try to redeem or sell quickly. The outcome depends on reserve liquidity, market confidence and the issuer’s ability to process redemptions under pressure.

Disclaimer: This article is for informational purposes only and is not financial advice. Cryptocurrency markets are volatile, and stablecoins, digital assets and related funds are subject to investment risk and regulatory change.