Real-World Asset Tokenization 2026: How RWAs Are Moving Traditional Finance Onchain

Crypto in 2026 is no longer defined only by speculative coins, meme-token cycles, or short-term trading narratives. One of the biggest structural shifts is the growth of real-world asset tokenization: the process of bringing traditional financial instruments onto blockchain rails. That includes U.S. Treasuries, money market funds, corporate bonds, private credit, commodities, real estate claims, and other tokenized assets that connect onchain finance with the offchain economy.

The trend is no longer theoretical. By February 2026, tokenized real-world assets reportedly grew to more than $24 billion in total value, after 266% growth during 2025. Tokenized U.S. Treasuries became the largest category at around $9.6 billion. That matters because it shows where crypto is maturing: not only toward new digital-native products, but toward blockchain-based infrastructure for familiar financial assets.

For beginners, investors, and active crypto users, real-world asset tokenization 2026 is important because it sits at the intersection of regulation, yield, liquidity, custody, and market access. It helps explain why banks, asset managers, and payment firms are paying attention to blockchain in a more practical way. It also shows why the RWA crypto trend is more serious than a passing narrative. This article is educational only and should not be treated as financial advice.

What real-world asset tokenization means

A real-world asset, or RWA, is an asset that exists outside a blockchain network. It may be a government bond, a share in a money market fund, a commodity holding, a corporate debt instrument, an invoice, a private credit exposure, or a legal claim connected to real estate. RWA tokenization means creating a blockchain-based token that represents some form of exposure, ownership interest, income right, or contractual claim related to that asset.

This distinction matters. A tokenized Treasury is not a government bond physically living on a blockchain. In most cases, a regulated issuer, fund, trustee, or special-purpose vehicle holds or manages the underlying asset in traditional financial infrastructure. The blockchain token is then used to represent a linked legal or economic right for the investor.

That is the main difference between crypto-native assets and tokenized real-world assets. Bitcoin and Ether are native to blockchain systems. They do not rely on an offchain custodian to prove they exist. By contrast, tokenized real-world assets depend on legal agreements, custodians, reserve management, disclosures, and compliance processes. If the offchain structure is weak, the token’s reliability is weak too.

Several parties usually make the system work:

- Issuers create and manage the tokenized product.

- Custodians or trustees hold or verify the underlying assets.

- Smart contracts issue, transfer, restrict, and sometimes redeem the tokens.

- Investors buy and hold the tokens through approved platforms, wallets, or intermediaries.

Because an RWA token represents a legal and economic arrangement rather than a purely digital object, documentation and regulation are central. Investors need to know what exactly the token represents, who controls the reserves, what rights they have, and under which jurisdiction those rights are enforceable. Without that legal layer, blockchain tokenized assets remain more marketing concept than durable financial product.

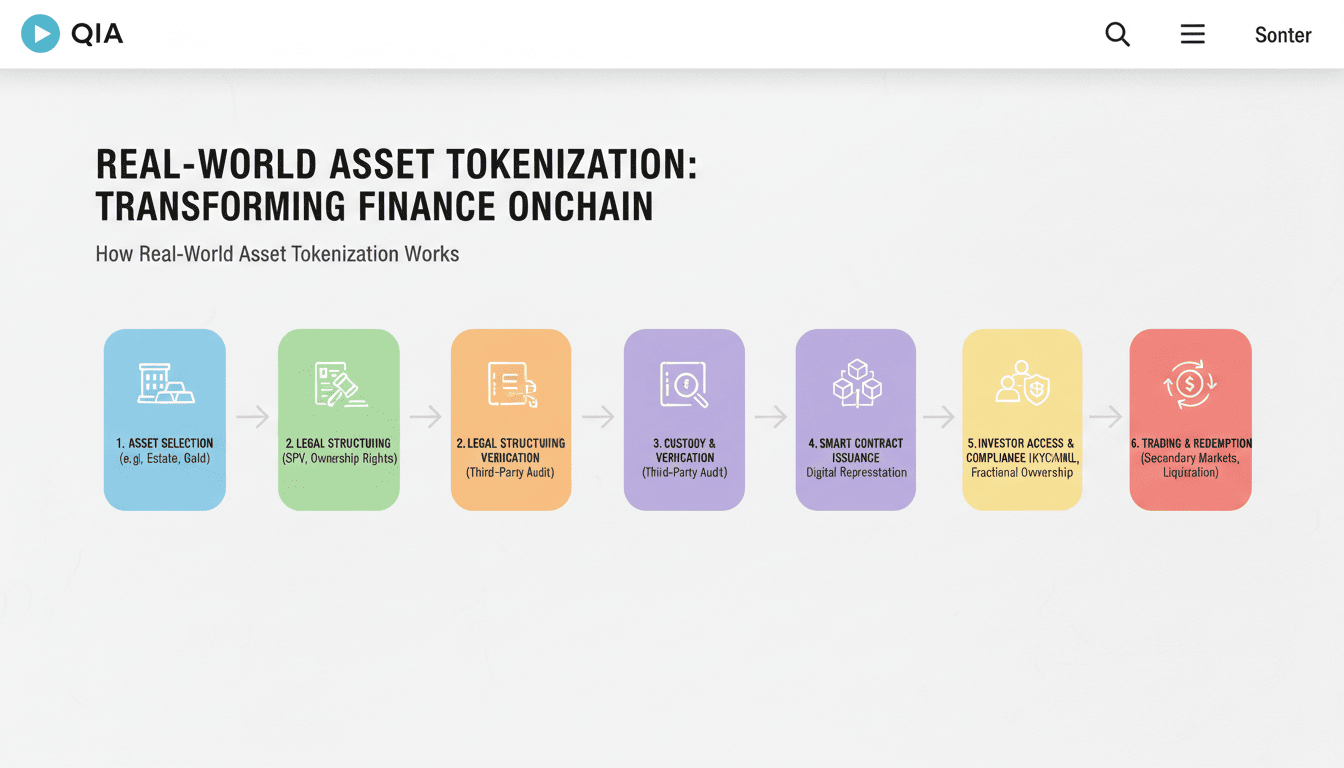

How RWA tokenization works in practice

For beginners, the easiest way to understand how RWA tokenization works is to think of it as a bridge between traditional financial assets and blockchain-based settlement. The token itself is only one piece of the structure. The legal, custody, and compliance layers matter just as much.

Asset selection

Not every asset is equally easy to bring onchain. In practice, the strongest early categories tend to be highly liquid, income-generating, and already understood by traditional markets. U.S. Treasuries and money market products fit that profile better than, for example, rare art or highly fragmented real estate rights. Assets with established pricing, regular cash flow, and lower valuation uncertainty are generally easier to tokenize responsibly.

Legal structuring

Next comes the core legal question: what does the token actually represent? Depending on the structure, the token may reflect direct ownership, beneficial interest in a fund, debt exposure, a revenue claim, a receivable, or another contractual right. This step is critical because two products can both be marketed as tokenized assets while giving investors very different rights in practice.

Custody and verification

Unlike crypto-native assets, blockchain real-world assets need a trusted offchain control system. The underlying bond, fund share, or commodity reserve must be held, administered, or verified by a custodian, trustee, bank, fund manager, or other regulated entity. Investors are therefore not just assessing code. They are also assessing the people and institutions behind the code.

Smart contract issuance

Once the legal and custody framework is in place, a smart contract can issue blockchain tokens. Those tokens may include transfer rules, whitelisting requirements, holding limits, compliance restrictions, and redemption functions. Smart contracts can also automate interest distributions, recordkeeping, or investor eligibility checks, which is one reason tokenized finance is attracting attention from institutions.

Investor access and compliance

Access is rarely open-ended. Many RWA products involve KYC, AML procedures, jurisdictional restrictions, and in some cases accredited-investor requirements. That means an investor may need to pass identity verification and use a specific platform before they can buy or transfer a tokenized security or fund product.

Trading, settlement, and redemption

After issuance, the token can potentially be transferred between approved users, used as collateral, or redeemed according to the issuer’s terms. This is where the tokenized asset process becomes attractive: settlement may be faster, transferability may be broader, and integration with onchain finance may be easier than in traditional systems. But these benefits only hold if the legal and operational structure is strong enough to support them.

In short, blockchain asset issuance for RWAs is not simply “putting a bond onchain.” It is building a regulated and verifiable wrapper that lets an offchain asset interact with digital infrastructure.

Why tokenized treasuries became the leading RWA category

Tokenized treasuries 2026 became one of the strongest search and investment themes for a simple reason: they combine familiar credit exposure with blockchain-based convenience. By early 2026, tokenized U.S. Treasuries reportedly reached about $9.6 billion, making them the largest RWA category. Products such as BlackRock’s BUIDL fund helped validate the market, with BUIDL reportedly accounting for roughly $1.7 billion in assets.

There are several reasons tokenized U.S. Treasuries moved ahead of more complex RWA segments.

- They are widely understood by institutions and corporate treasury teams.

- They generate yield, which matters in both crypto and traditional finance.

- They are easier to price and account for than illiquid assets such as private real estate.

- They can serve as a relatively lower-risk parking place compared with volatile crypto assets.

This is especially important in onchain markets. Stablecoin issuers, funds, DAOs, and DeFi participants often hold idle capital that they want to keep liquid while still earning yield. Tokenized Treasury products can fill that role better than non-yielding stablecoin balances alone. For institutions exploring onchain finance, Treasuries are also a comfortable starting point because the underlying asset class is already a core part of global financial infrastructure.

Another reason for growth is treasury management. A company or crypto-native organization may want exposure to short-duration government securities without relying entirely on slower banking or broker workflows. A tokenized Treasury product can, depending on structure, make subscriptions, transfers, collateralization, and operational reporting more efficient.

Still, tokenized Treasuries are not risk-free. Investors should pay attention to issuer quality, legal structure, redemption conditions, and platform access rules. There is also liquidity risk: an onchain token may exist, but that does not guarantee a deep and efficient secondary market. Regulatory access can also vary by country and investor type. So while products like BlackRock BUIDL and other RWA treasuries have added legitimacy to the market, users still need to study the details before treating them like direct Treasury ownership.

Main types of tokenized real-world assets

The RWA market is broader than Treasuries. Understanding the main types of tokenized assets helps investors see where tokenization works best today and where the market is still early.

Tokenized U.S. Treasuries

This remains the strongest category in 2026. Treasuries are liquid, yield-bearing, well-understood, and relatively simple to integrate into institutional workflows. They are often the first example people point to when discussing serious blockchain real-world assets.

Tokenized money market funds

Tokenized money market funds are familiar financial products adapted to blockchain-based ownership, transfer, and settlement. They appeal to institutions and treasury managers because they can offer low-volatility cash management exposure with more programmable infrastructure. In many ways, they represent the bridge between stablecoin-like utility and traditional fund management.

Tokenized corporate bonds

Tokenized bonds are a natural fit because bonds already have defined maturity dates, coupon structures, and cash-flow expectations. That makes them easier to document and model than many other asset classes. Onchain issuance can also improve settlement efficiency and transparency for certain participants, which is why corporate bond experiments continue to attract attention.

Tokenized private credit

Private credit is one of the more talked-about RWA categories because yield can be attractive, but risk is also materially higher. These products may involve lending to businesses or borrowers outside public markets. They are generally less liquid, harder to value, and more sensitive to underwriting quality than Treasuries or money market funds. Investors need to be especially careful with legal rights, default procedures, and reserve disclosures.

Tokenized commodities

Tokenized commodities bring physical asset exposure into digital form, with gold being the clearest example for retail users. Gold-backed tokens are easy to understand because the underlying narrative is simple: a reserve-backed asset with familiar market demand. According to the briefed market context, tokenized commodities continue to expand, with gold dominating tokenized commodity value.

Tokenized real estate

Tokenized real estate is often promoted as a fractional ownership story. In theory, tokenization can lower investment minimums and make ownership claims easier to divide and transfer. In practice, legal complexity remains a major challenge. Property rights, local laws, taxes, debt claims, and transfer restrictions can make this category much harder than the marketing suggests. Liquidity can also remain weak even if the ownership is split into tokens.

Tokenized equities

Tokenized equities are becoming an important retail-facing trend because stocks are far easier for many users to understand than niche DeFi instruments. DWF Labs highlights tokenized equities as a possible retail demand engine for RWA adoption in 2026. If infrastructure and regulation improve, tokenized stocks may become a major gateway into onchain finance for mainstream investors.

Each category has different legal and operational requirements. The broad takeaway is that not all tokenized securities are equally mature. Treasuries and money market products currently look more institutional and practical, while real estate and private credit still come with heavier structural complexity.

Why institutions are moving into RWA tokenization

Institutional participation is one of the clearest signs that RWA tokenization is more than another short-lived crypto cycle. Banks, asset managers, fund groups, and market infrastructure providers are exploring tokenized finance because it applies blockchain technology to familiar assets and known workflows. Instead of inventing value from scratch, they are using blockchain as a new operating layer for assets markets already understand.

According to the market examples in the brief, firms such as Franklin Templeton, JPMorgan, Fidelity, and Apollo launched or expanded tokenized products, while Siemens issued a €300 million corporate bond onchain. That kind of activity matters because institutions are usually slow, process-heavy adopters. They do not move into a sector simply because it is fashionable on social media.

Why are they interested?

- Yield and familiarity: Regulated, income-generating assets are easier to approve internally than speculative digital assets.

- Operational efficiency: Blockchain settlement can reduce reconciliation friction and shorten some parts of the transaction process.

- Programmable compliance: Transfer restrictions and investor permissions can be built into token design.

- Collateral utility: Tokenized assets may become easier to mobilize across digital markets.

That said, tokenization is not replacing traditional finance overnight. Most institutions are starting with narrow, controlled use cases such as internal settlement tests, fund share tokenization, treasury tools, or limited collateral applications. Adoption is likely to move gradually through back-office improvements and regulated product wrappers before it reaches anything close to mass-market scale.

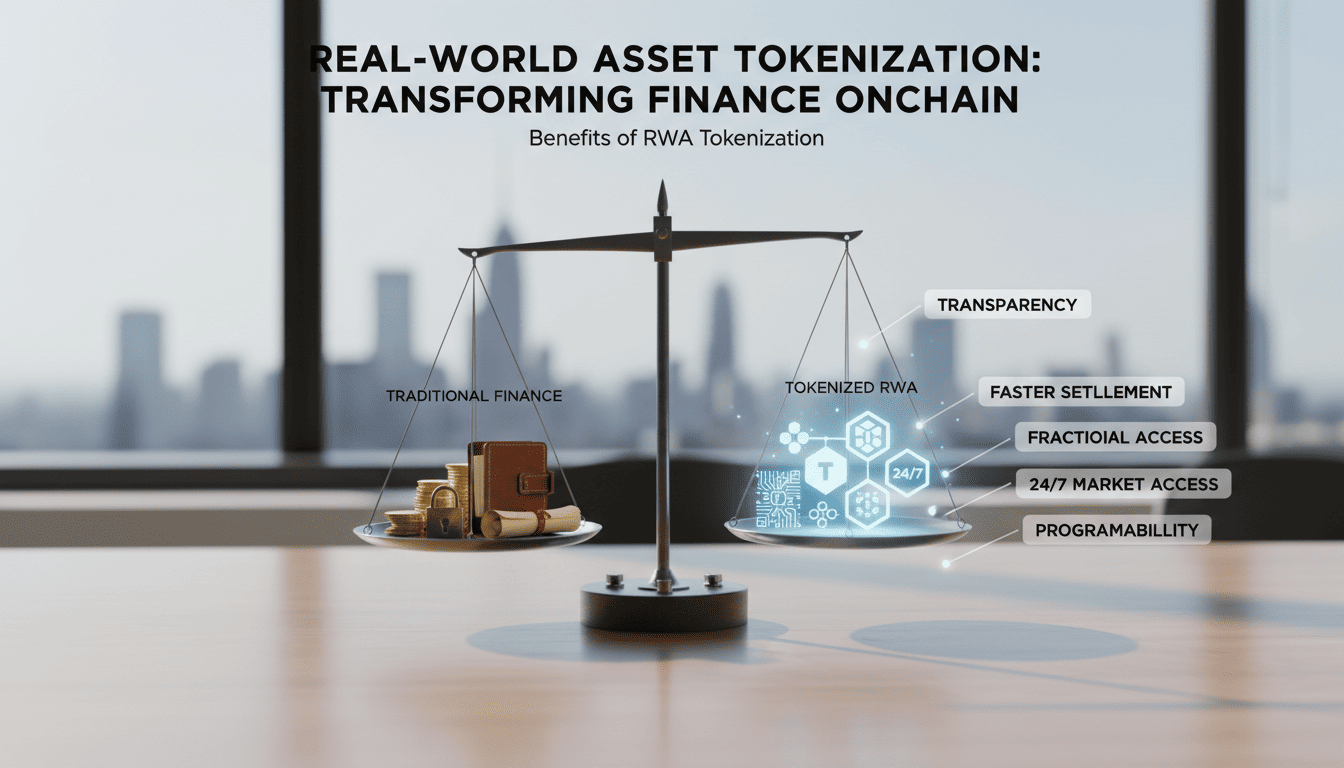

Benefits of RWA tokenization for investors and markets

The appeal of RWA tokenization is not that it magically makes every asset better. The real value lies in how blockchain infrastructure can change access, transfer, transparency, and programmability around existing assets.

Fractional access

Some tokenized assets can lower minimum investment sizes. That may make certain products easier to access for smaller investors, family offices, or digital-native users who do not want to move through full traditional brokerage pipelines for every allocation. Fractional access is especially relevant for assets that have historically required large ticket sizes.

Faster settlement

Blockchain settlement can reduce delays compared with slower traditional post-trade processes. While not every tokenized product settles instantly in a legal sense, blockchain rails can improve transfer speed, ownership recording, and operational coordination between counterparties.

Potential 24/7 market access

Traditional financial markets usually run within limited opening hours, while blockchain networks are always live. That does not mean every tokenized security can trade freely around the clock, but onchain infrastructure creates the possibility of broader transferability and more flexible market access where regulations and platform rules allow it.

Transparency

Onchain records can make movements, balances, and transaction history more visible. In well-designed systems, investors may also benefit from reserve reporting and proof-related disclosures. Transparency is not automatic, but tokenization can make it easier to build auditability into the product design.

Programmability

This is one of the strongest advantages of tokenized assets. Smart contracts can automate compliance, transfer permissions, payment flows, and certain operational tasks. That can reduce manual processing and create new financial workflows that are harder to build in legacy systems.

Composability

In onchain finance, composability means an asset can interact with other protocols and services. According to DWF Labs’ summary of industry thinking, the strongest RWA products in 2026 are expected to be liquid, tradable, composable, and usable as collateral across DeFi systems. That is the bigger long-term opportunity: not just putting assets on a blockchain, but making them work inside a broader financial network.

The benefits are real, but they depend heavily on the quality of the issuer, the legal structure, and the secondary-market infrastructure. Good token design does not eliminate bad underwriting or poor governance.

Risks and limitations investors should understand

A balanced view of RWA tokenization risks is essential. Real-world asset tokenization is promising, but it is not frictionless and it is not inherently safe just because it uses blockchain. In fact, it combines the risks of both traditional finance and digital asset infrastructure.

Liquidity risk

A token can be tradable in theory while remaining illiquid in practice. Many tokenized assets still have shallow secondary markets, limited market makers, or narrow investor access. Uneven liquidity remains one of the main structural limitations across the RWA market.

Legal and regulatory risk

Tokenized securities regulation differs across jurisdictions. A product that is accessible in one country may be restricted in another. Regulators may classify tokenized funds, bonds, or claims differently depending on local law. Investors should never assume a product is universally allowed just because it is visible onchain.

Custodian and issuer risk

The token is only as strong as the real-world structure behind it. If the issuer, custodian, trustee, or fund administrator fails, investors may face delays, legal disputes, or loss of access. This is one of the biggest differences between crypto-native assets and tokenized real-world assets.

Smart contract risk

Code can fail. Bugs, exploits, poor upgrade controls, or governance mistakes can affect transferability, redemption, accounting, or collateral integration. Even a fully legitimate underlying asset can become problematic if the blockchain implementation is weak.

Redemption risk

One of the most practical tokenized asset risks is redemption uncertainty. Investors need to know who can redeem, on what schedule, in what size, and under what conditions. If redemption is slow, gated, expensive, or available only to certain investors, the token may trade at a discount or become operationally awkward.

Oracle and pricing risk

RWAs often need offchain pricing data. In DeFi collateral systems, inaccurate valuations can lead to poor risk management, bad liquidations, or false assumptions about solvency. Reliable data feeds and conservative collateral rules matter far more than promotional language.

Retail misunderstanding

Many beginners hear “Treasuries,” “funds,” or “real-world assets” and assume those products must be safer than crypto tokens. That is not always true. The underlying asset may be familiar, but the wrapper may still involve legal, technical, and liquidity complications. Investors should evaluate the full structure, not just the headline asset class.

The briefed market view also notes fragmented standards and limited participation beyond institutions. That means the sector may continue growing while still remaining uneven in quality, market depth, and user experience. Investors should approach it with curiosity, but not with blind trust.

RWA tokenization vs traditional investing

The simplest way to frame RWA vs traditional finance is this: tokenization is not automatically better. It is a new infrastructure layer that may improve certain workflows and asset uses, while traditional markets still dominate in scale, liquidity, and user familiarity.

The table below summarizes the main differences.

| Category | Traditional investing | Tokenized investing |

|---|---|---|

| Access | Usually through brokers, banks, or fund platforms | Through wallets, digital platforms, or regulated token issuers |

| Settlement | Often slower and more layered | Potentially faster onchain transfers and record updates |

| Market hours | Usually limited by exchange or banking hours | Potentially broader transferability, depending on product rules |

| Ownership records | Centralized registries and intermediaries | Blockchain-based records plus offchain legal documentation |

| Compliance | Broker-led and institution-led | Platform-led and sometimes embedded in smart contracts |

| Liquidity | Usually deeper in public markets | Still developing for many RWA products |

| User experience | More familiar for mainstream investors | Often more flexible, but more complex |

The comparison shows why tokenized securities vs stocks is not a simple winner-loser question. Public equities and bonds still benefit from mature infrastructure, broad regulation, and deep secondary markets. Tokenized investing may offer speed, programmability, and composability, but mainstream usability is still catching up.

Why stablecoins and RWAs are closely connected

To understand modern onchain finance, it helps to see stablecoins as the cash layer and RWAs as the yield layer. Stablecoins showed that tokenized value can move globally at meaningful scale. According to Stripe, stablecoin transfer volume reached $27.6 trillion in 2024, exceeding the combined transaction volume of Visa and Mastercard. That scale created a practical foundation for broader blockchain-based financial products.

Stablecoins and RWA growth are linked in several ways.

- Stablecoins are widely used to subscribe to, settle, and redeem tokenized asset products.

- Stablecoin issuers often hold Treasury-related assets as reserves or reserve-like exposure.

- Onchain users with idle stablecoin balances want yield-bearing alternatives.

- Tokenized money market products can function as treasury-management tools within digital ecosystems.

This is why tokenized treasuries stablecoins is such an important combined theme. A stablecoin may serve as the transactional medium, while tokenized Treasuries or money market funds serve as the capital-efficiency layer behind it. That arrangement matters for exchanges, DeFi protocols, payment companies, and treasury teams trying to manage onchain capital more actively.

In other words, stablecoins proved that blockchain can move dollars. RWAs are trying to prove that blockchain can also move regulated yield-bearing assets in a reliable and compliant way.

How RWAs could affect crypto exchanges and trading platforms

If tokenized assets continue growing, crypto exchanges and digital asset platforms may evolve beyond Bitcoin, Ethereum, and altcoins into broader financial marketplaces. That does not mean every exchange will suddenly list tokenized stocks, bonds, or funds. But it does mean platform differentiation could increasingly depend on custody standards, compliance tools, supported jurisdictions, product depth, and integration with regulated issuers.

For users, that creates both opportunity and complexity. A platform that is good for spot crypto trading may not be the best place to access or store tokenized securities. Some venues may focus on institutional distribution, while others may target retail access to tokenized equities or commodities. Before choosing where to trade or research tokenized assets, users should compare fees, supported assets and platform features through a reliable crypto exchange comparison resource.

The rise of RWA trading platforms could also push exchanges toward more finance-like services, including yield products, collateral management, tokenized settlement tools, and cross-market analytics. Over time, the difference between a crypto platform and a digital brokerage may become less clear, especially if tokenized asset exchanges gain regulatory support in more regions.

Still, users should not assume a platform listing a tokenized product has solved all the hard parts. Investors need to understand where the legal claim sits, who handles redemption, and whether they are buying a regulated instrument or simply a synthetic representation.

How beginners can research tokenized assets safely

For newcomers, the biggest mistake is assuming that “real-world” means “low-risk.” A better approach is to use a basic due-diligence checklist before buying any tokenized product. New investors who are still learning how digital assets work can also explore CoinixPro’s crypto guides for beginners before moving into more complex products such as RWAs.

Here is a practical checklist for how to research tokenized assets safely:

- Check who issued the token. Is the issuer known, regulated, and transparent?

- Check what the token legally represents. Ownership, fund share, debt claim, revenue right, or synthetic exposure are not the same thing.

- Check whether the product is regulated. The answer may differ by country and investor type.

- Check the custodian or reserve structure. Who actually holds the underlying asset?

- Check redemption terms. Can you redeem easily, and on what schedule?

- Check liquidity and trading volume. A token can exist onchain while still being hard to exit.

- Check smart contract audits. Look for public security reviews and governance transparency.

- Check fees. Management, minting, redemption, spread, and platform fees all matter.

- Check tax implications. Yield, transfers, and redemptions may trigger tax events.

- Avoid assuming tokenized means risk-free. Structural quality matters more than branding.

This checklist is especially useful for RWA investing for beginners. The goal is not to master every legal technicality, but to avoid treating tokenized products like simple app-based versions of traditional assets. The wrapper can change the risk profile significantly.

Best use cases for RWA tokenization in 2026

The most compelling RWA use cases are practical, not theoretical. The technology matters when it solves a real operational or market problem better than legacy systems.

Treasury management

Businesses, DAOs, funds, and crypto-native organizations often hold large cash balances or stablecoin reserves. Tokenized Treasury or money market products can provide a way to manage idle capital while keeping it connected to digital infrastructure. This may become one of the most durable institutional use cases in 2026.

DeFi collateral

Tokenized treasury collateral is attractive because it can bring lower-volatility, yield-bearing assets into onchain lending and risk systems. If protocols can handle pricing, liquidation, and compliance correctly, tokenized Treasuries or funds may improve the quality of collateral compared with purely speculative tokens.

Cross-border access

Depending on local laws, tokenization may help some investors access assets that were previously difficult to reach through standard brokerage channels. This does not remove regulatory barriers, but it may simplify product distribution in certain global markets where traditional access has been fragmented or expensive.

Institutional settlement

Banks and asset managers may use blockchain rails to streamline issuance, transfer, reporting, and settlement. This use case is often less visible to retail users, but it may be one of the most important long-term drivers of adoption because it addresses real back-office friction.

Tokenized equity trading

Tokenized stocks 2026 could become a major retail narrative because equities are familiar, intuitive, and easier to compare than many DeFi yield structures. If regulation, custody, and market infrastructure improve, tokenized equities may become one of the clearest consumer-facing RWA products.

The strongest pattern across all these use cases is utility. The market will likely reward products that combine legal clarity, tradability, and real operational usefulness, not just products that can be described as “onchain.”

RWA tokenization by region: US, Europe, Singapore, and global markets

The global RWA market is developing unevenly because regulation, investor access, and financial infrastructure differ by region. Geography still matters a great deal for tokenized assets.

United States

The US remains central because of the scale of Treasury markets, the role of dollar-based products, and the influence of major asset managers. Much of the current momentum around tokenized funds and Treasuries is tied to US financial instruments. At the same time, securities regulation remains one of the key constraints shaping how RWA tokenization US products are distributed and who can access them.

Europe

Europe is important because regulatory clarity and structured digital asset frameworks can create a more defined environment for issuance and settlement experiments. Corporate bond tokenization and institutional pilots have helped Europe stay relevant in this space. For many observers, tokenized assets Europe becomes a question of how regulatory structure can support market confidence without slowing innovation too much.

Singapore

Singapore is highly relevant to digital asset infrastructure, especially for regulated financial experimentation, fund distribution, and institutional blockchain initiatives. It often appears in discussions about compliant tokenization because it combines financial-market sophistication with active digital asset policy development. That makes tokenized funds Singapore a useful regional lens for understanding how regulated adoption might scale in Asia.

Global markets

Outside the largest financial centers, RWA adoption may become especially attractive where traditional market access is limited, expensive, or inefficient. That said, local rules will determine how much retail participation is possible. In many regions, institutional and professional investors are still likely to remain the main users in the near term.

What comes next for RWA tokenization

The future of RWA tokenization is likely to be more practical and more selective than early marketing suggested. Growth will probably continue, but the strongest products will be the ones that solve real financial problems rather than simply adding blockchain branding to existing assets.

The next phase likely includes:

- More tokenized Treasuries and money market products

- More regulated fund structures and institutional distribution

- Improved secondary-market infrastructure

- Broader tokenized equities experimentation

- Deeper integration with DeFi collateral systems

- More compliance logic built into smart contracts

- Better institutional-grade custody and reporting

DWF Labs makes an important point for RWA trends 2026: announcements alone are no longer enough. A successful tokenized asset must be priced properly, tradable in real conditions, composable across useful systems, and safe enough to be used as collateral where appropriate. That is a much higher bar than simply launching a token.

Retail adoption is also likely to be gradual rather than explosive. Many users still find traditional investing interfaces easier than wallets, whitelists, and token custody. Over time, however, front-end improvements could hide some of that complexity. If that happens, the line between traditional products and onchain wrappers may become less visible to the average investor.

In that sense, tokenized finance future is less about replacing every old system and more about rebuilding parts of the financial stack on more programmable rails. The winners will probably be products that make markets measurably better, not just more digital.

Should investors pay attention to RWA tokenization?

Yes, because real-world asset tokenization is one of the most serious crypto developments in 2026. The strongest categories so far are tokenized Treasuries, money market funds, and other institutionally structured products, not purely speculative experiments. The appeal is clear: faster settlement, programmable ownership, potential fractional access, and better compatibility with onchain finance.

But the risks are just as important. Liquidity can be thin, redemption terms can be restrictive, regulation varies by region, and the legal reliability of the token depends on the structure behind it. Readers who want to compare broader crypto services before exploring new asset categories can also review CoinixPro’s coverage of best crypto platforms.

The smartest approach is to treat RWAs as an important trend worth understanding, not as an automatic investment opportunity. Education first, due diligence second, participation last.

Frequently asked questions about real-world asset tokenization

What is real-world asset tokenization?

Real-world asset tokenization is the process of turning exposure to an offchain asset into a blockchain-based token. The token may represent ownership, beneficial interest, debt exposure, income rights, or another contractual claim. The key point is that the underlying asset exists outside the blockchain, while the token provides a digital wrapper around related rights.

What are examples of tokenized real-world assets?

Common examples include tokenized U.S. Treasuries, tokenized money market funds, tokenized corporate bonds, tokenized gold and other commodities, tokenized private credit, tokenized real estate interests, and tokenized equities. Not all of these categories are equally mature, but together they define the broader RWA market.

Are tokenized assets the same as cryptocurrencies?

No. Cryptocurrencies such as Bitcoin or Ether are crypto-native assets created directly on blockchain networks. Tokenized assets represent offchain assets or legal claims tied to real-world financial instruments, reserves, or rights. That means tokenized products usually depend more heavily on issuers, custodians, legal agreements, and regulation.

Why are tokenized Treasuries popular in 2026?

Tokenized treasuries are popular because they combine a familiar asset class with blockchain-based settlement and transfer features. They appeal to institutions, treasury managers, and onchain users looking for yield-bearing products that are generally less volatile than many crypto assets. Their pricing and legal structure are also easier to understand than more experimental RWA categories.

Are tokenized real-world assets safe?

They may be more familiar than speculative tokens, but they are not automatically safe. Investors still face legal risk, issuer risk, custodian risk, liquidity risk, redemption risk, and smart contract risk. A token backed by a real-world asset can still perform badly or create access problems if the underlying structure is weak.

Can retail investors buy tokenized assets?

Sometimes, yes. Access depends on the type of asset, the rules of the platform, and local regulation. Some tokenized products are open only to institutional or accredited investors, while others are designed with broader access in mind. Jurisdiction remains one of the most important limits on retail participation.

How do RWAs connect with DeFi?

RWAs connect with DeFi through collateral, lending, settlement, and yield-bearing onchain products. For example, tokenized Treasuries may be used in lending markets if the protocol can handle compliance and valuation issues. Stablecoins often act as the payment and settlement layer, while RWAs bring offchain yield into onchain systems.

What is the biggest risk in RWA tokenization?

There is no single universal risk, but the biggest issues tend to be liquidity, regulatory uncertainty, and the gap between the onchain token and the actual legal asset. If that bridge is poorly designed, investors may discover that the token is less enforceable, less redeemable, or less liquid than expected.

Will RWA tokenization replace traditional finance?

Not in the near term. It is more realistic to think of tokenization as an additional infrastructure layer rather than a full replacement for traditional finance. Public markets, banks, brokers, and fund platforms still dominate in scale and usability. Tokenization may gradually improve how certain assets are issued, transferred, settled, and used as collateral.

Is RWA tokenization a good topic to follow in 2026?

Yes. It is one of the most important themes in digital assets because it combines institutional relevance, real financial products, and growing onchain utility. Compared with many crypto narratives, real-world asset tokenization 2026 is less about hype and more about whether blockchain infrastructure can improve actual capital markets.

Real-world asset tokenization is worth watching because it links the familiar logic of traditional finance with the flexibility of blockchain networks. The market is still early, and the details matter, but the direction is clear: Treasuries, funds, bonds, and other assets are increasingly moving onchain. For investors, the best response is not blind enthusiasm or blanket skepticism. It is careful research, realistic expectations, and a strong understanding of how the legal and technical pieces fit together.